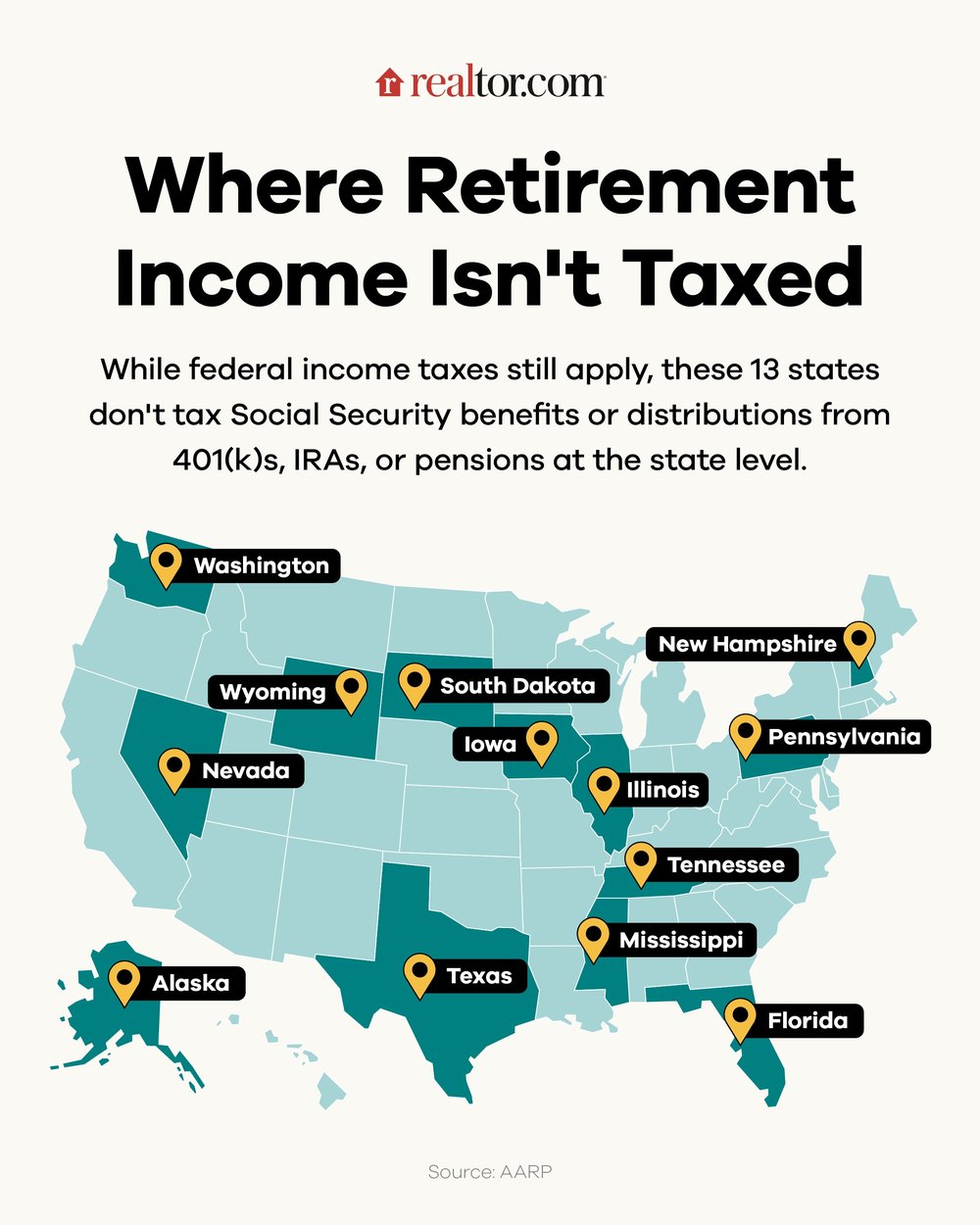

Americans Are Draining Their Retirement Savings to Keep Their Homes

Across the United States, a growing number of homeowners are making a desperate financial decision: pulling money out of their 401(k) accounts early to cover mortgage payments and avoid foreclosure. While it may feel like a lifeline in a moment of crisis, financial experts warn that this move can permanently derail your retirement — and in many cases, it doesn't even solve the underlying problem.

New data from Fidelity Investments reveals that the average 401(k) balance fell by 4% to $141,000 at the start of 2026. The average individual retirement account (IRA) balance dropped by the same margin to $131,380 in the first quarter of 2026. These declines are not just the result of market volatility — they reflect a troubling pattern of Americans withdrawing funds they cannot afford to lose.

What Are Hardship Withdrawals and Why Are They Rising?

A hardship withdrawal is a provision under IRS rules that allows 401(k) participants to take money out of their retirement accounts before the standard retirement age of 59½. To qualify, the need must be described as "immediate and heavy" — a high bar, but one that is increasingly being met by everyday Americans struggling to keep up with housing costs.

According to Vanguard's 2026 report on Americans' savings habits, 6% of people enrolled in Vanguard 401(k) plans made hardship withdrawals in 2025. That number represents a sharp increase from 5% in 2024 and 3.6% in 2023. The trend is unmistakable: more people are turning to their retirement nest eggs as a financial emergency fund, and the most common reason cited is making a rent or mortgage payment to avoid foreclosure or eviction.

This is not a fringe behavior. Millions of Americans are now walking a tightrope between keeping a roof over their heads and securing their financial future, and many are choosing the roof — at a steep long-term cost.

The Real Cost of Tapping Your 401(k) Early

Many people underestimate just how expensive an early 401(k) withdrawal actually is. When you withdraw money before age 59½, the financial consequences stack up quickly:

- Federal income tax: The withdrawn amount is added to your ordinary income for the year, potentially pushing you into a higher tax bracket.

- 10% early withdrawal penalty: On top of income taxes, the IRS imposes a 10% penalty on the amount withdrawn unless a specific exception applies.

- Lost compound growth: Perhaps the most damaging consequence is the one people rarely account for — the long-term compounding that money would have generated over decades. A $20,000 withdrawal today could cost you $100,000 or more by the time you retire.

- Reduced retirement security: Every dollar taken out is a dollar that will no longer be working for your future, leaving you more financially vulnerable in old age.

For someone in a 22% federal tax bracket, a $10,000 hardship withdrawal effectively nets only around $6,800 after taxes and penalties. That's a brutal exchange rate for emergency cash.

Why the Economic Pressure Isn't Going Away Soon

The surge in hardship withdrawals doesn't exist in a vacuum. It is the direct result of a prolonged period of financial stress affecting American households. Inflation rose 3.8% compared to the previous year, squeezing household budgets that were already stretched thin. Mortgage rates remain elevated, making monthly payments significantly higher than they were just a few years ago. Housing costs have not meaningfully declined in most major markets, and geopolitical instability — including the ongoing conflict in the Middle East — continues to cast uncertainty over energy prices and the broader economy.

For many homeowners, especially those who purchased homes in the past two to three years at higher prices and higher rates, the math simply doesn't work anymore without some form of emergency relief. Unfortunately, that relief often comes in the form of retirement savings that should never be touched prematurely.

Safer Alternatives to Raiding Your Retirement Account

Before you take a hardship withdrawal from your 401(k), it is worth exhausting every other available option. There are several alternatives that carry far less long-term damage to your financial health:

- 401(k) loan: Many plans allow you to borrow from your own account and repay it with interest over time. Unlike a withdrawal, a loan does not trigger income taxes or penalties as long as it is repaid on schedule.

- Mortgage forbearance: Contact your loan servicer directly. Federal programs and lender-specific options may allow you to pause or reduce payments temporarily without damaging your credit or triggering foreclosure.

- HUD-approved housing counseling: The U.S. Department of Housing and Urban Development offers free or low-cost counseling services that can help you negotiate with your lender and identify assistance programs you may qualify for.

- State and local assistance programs: Many states have homeowner relief programs designed specifically for people at risk of foreclosure. These can include grants, deferred payment programs, or zero-interest loans.

- Personal loans or home equity lines of credit: While not ideal, these options typically carry lower effective costs than the combined tax hit and penalty of a 401(k) withdrawal.

What This Trend Means for Long-Term Retirement Security

The growing reliance on 401(k) hardship withdrawals is a warning signal for the broader retirement landscape in America. For decades, the shift from employer-funded pensions to employee-directed retirement accounts placed the burden of retirement savings squarely on individuals. That system only works if those savings remain intact until retirement.

When a significant and growing share of savers begins treating their 401(k) as an emergency fund, it creates a compounding crisis: people who need retirement income the most — those who faced the greatest economic hardship during their working years — will also have the least saved when they reach old age. This dynamic risks intensifying poverty among future retirees and increasing pressure on social safety nets.

Protect Your Retirement: Make the Hard Choice Now

If you are facing mortgage difficulties, the instinct to protect your home at all costs is understandable. But cashing out your retirement savings may trade one crisis for a larger, slower-moving one. Before making any decision, speak with a certified financial planner or a HUD-approved housing counselor who can help you assess all your options with clear eyes.

Your home matters. But so does your financial future. The most dangerous move you can make with your 401(k) is treating it like a checking account — because once that money is gone, the decades of compounding growth it would have generated are gone with it.