China's Light Vehicle Market Records Sharp 24% Year-on-Year Decline in April 2026

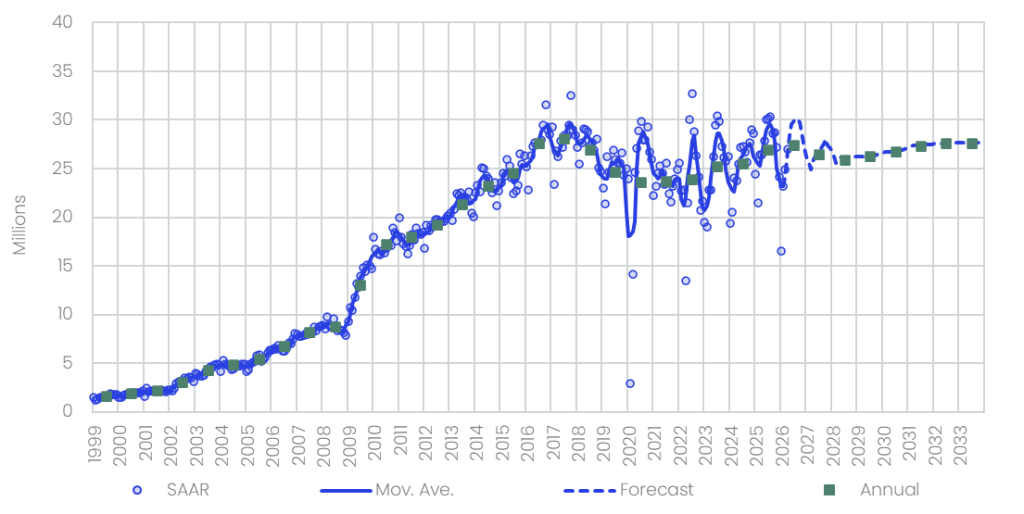

China's automotive sector faced one of its most challenging months in recent memory in April 2026, with total Light Vehicle (LV) sales tumbling to 1.6 million units — a steep 24% year-on-year (YoY) decline. The latest data paints a sobering picture for an industry that had only recently been buoyed by government stimulus measures and a booming electric vehicle segment. The numbers suggest that structural headwinds, including tightened subsidy policies and softer domestic consumer sentiment, are now beginning to bite in a meaningful way.

According to analysts tracking the market, the seasonally adjusted annualized rate (SAAR) for April stood at 21.0 million units, down 20.7% from the same period last year. When viewed across the broader January-to-April window, the situation looks equally grim, with cumulative LV sales falling 22% YoY to just 6.2 million units. These figures confirm that April was not an isolated anomaly but rather the continuation of a downward trend that has gathered pace throughout the first third of 2026.

Passenger Vehicles Bear the Brunt of the Slowdown

The Passenger Vehicle (PV) segment proved to be the primary drag on overall market performance, contracting by 25% YoY to 1.4 million units in April. This is a striking reversal from the stronger sales trajectory that characterized much of 2024 and 2025, periods when generous government trade-in incentives and rising NEV penetration helped propel the market forward.

The Light Commercial Vehicle (LCV) segment, while not immune to broader market pressures, demonstrated relative resilience by comparison. LCV sales fell by a comparatively modest 12% YoY to approximately 209,000 units. Although a double-digit decline is far from encouraging, the more contained contraction suggests that business-related vehicle demand has held up somewhat better than consumer-driven passenger car purchases — at least in the near term.

The Subsidy Policy Shift: A Critical New Headwind

Perhaps the most consequential driver of April's dramatic sales shortfall is a fundamental change in how China structures its vehicle trade-in subsidies. In 2025, the government operated a straightforward, flat-amount subsidy program that offered consumers a fixed CNY 20,000 (approximately $3,000) rebate on New Energy Vehicles (NEVs) and CNY 15,000 (approximately $2,200) on Internal Combustion Engine (ICE) vehicles. The simplicity and generosity of this scheme made it a powerful purchase incentive across a wide range of price points.

The 2026 program, however, has shifted to a percentage-of-purchase-price model, and this change has materially altered the incentive landscape. Under the new rules, NEV buyers receive a subsidy worth 12% of the purchase price, capped at CNY 20,000, while ICE buyers receive 10%, capped at CNY 15,000. On paper, the maximum subsidy amounts remain unchanged. In practice, however, the shift to a percentage-based model means that buyers of lower-priced vehicles — a significant portion of China's mass market — receive considerably less support than they did under the previous flat-rate structure.

For example, a consumer purchasing a NEV priced at CNY 80,000 would have received the full CNY 20,000 flat subsidy in 2025. Under the 2026 program, that same buyer would receive only CNY 9,600 — a reduction of more than 50%. This erosion of effective subsidy value for budget-conscious consumers has acted as a direct demand suppressant, particularly in the entry-level and lower-mid-range vehicle segments that dominate China's retail automotive market.

NEV Demand Implications: A Market Under Pressure

The structural shift in subsidy design carries particularly significant implications for China's NEV sector, which has been central to the country's broader automotive ambitions. While NEVs had been riding a wave of consumer enthusiasm and policy tailwinds in recent years, the recalibration of subsidies toward a percentage-based model risks undermining the affordability advantage that many entry-level electric models had built up. Automakers targeting the mass market with competitively priced EVs may now need to reconsider their pricing strategies or risk a further softening in consumer uptake.

That said, premium NEV buyers — those purchasing vehicles priced at or above approximately CNY 167,000 — will continue to benefit from the full capped subsidy amount, meaning the impact is far from uniform across the market. The divergence between value-segment and premium-segment performance could become an increasingly prominent feature of China's NEV landscape over the coming months.

Export Surge Helps Anchor Production Despite Domestic Weakness

While domestic sales data tells a story of contraction, China's vehicle production figures have remained comparatively anchored, held up in large part by a continued surge in automotive exports. Chinese automakers have been aggressively expanding their international footprint, with exports to emerging markets in Southeast Asia, the Middle East, Latin America, and Eastern Europe helping to compensate for softening home demand. This export-driven production resilience is significant: it means that factory utilization rates and supply chain activity have not collapsed in step with domestic retail sales, providing a partial buffer for the broader industry.

However, relying on export markets as a structural counterweight to domestic weakness carries its own risks. Rising trade tensions, increasing tariff barriers in key export destinations, and intensifying competition from local manufacturers in some overseas markets could limit how much further China's export growth can travel as a safety valve for domestic overproduction.

What This Means for the Road Ahead

The combination of tighter subsidy mechanics, cautious consumer spending, and an uncertain global trade environment means the Chinese automotive market faces a challenging path through the remainder of 2026. Industry analysts will be watching closely to see whether the government responds with further policy adjustments to shore up domestic demand, particularly in the NEV segment where strategic long-term goals remain firmly intact.

- China LV sales fell 24% YoY to 1.6 million units in April 2026, with the SAAR down to 21.0 million units.

- Passenger vehicle sales contracted 25% YoY, while LCV sales declined a relatively contained 12% YoY.

- Cumulative January-April sales dropped 22% YoY to 6.2 million units, confirming sustained market weakness.

- The shift from flat-rate to percentage-based trade-in subsidies has meaningfully reduced incentives for buyers of lower-priced vehicles.

- Strong export activity is helping sustain production output even as domestic retail demand falters.

For automakers, suppliers, and investors with exposure to the Chinese market, April's figures serve as a clear signal that the demand environment has materially changed. Strategies built around the consumption dynamics of 2024 and 2025 may need revisiting. Whether policymakers intervene decisively to reinvigorate consumer confidence — or allow the market to find its own floor — will be the defining question for China's automotive sector in the months ahead.