Homebuilder Confidence Falls Again in June 2026 as Mortgage Rates and Costs Weigh Heavy

After a brief uptick in May offered a glimmer of hope for the housing industry, homebuilder confidence reversed course in June 2026, sliding two points amid a perfect storm of financial pressures. Elevated mortgage rates, stubbornly high material costs, and persistent affordability headwinds are once again squeezing builders across the country, raising fresh concerns about the near-term outlook for new home construction.

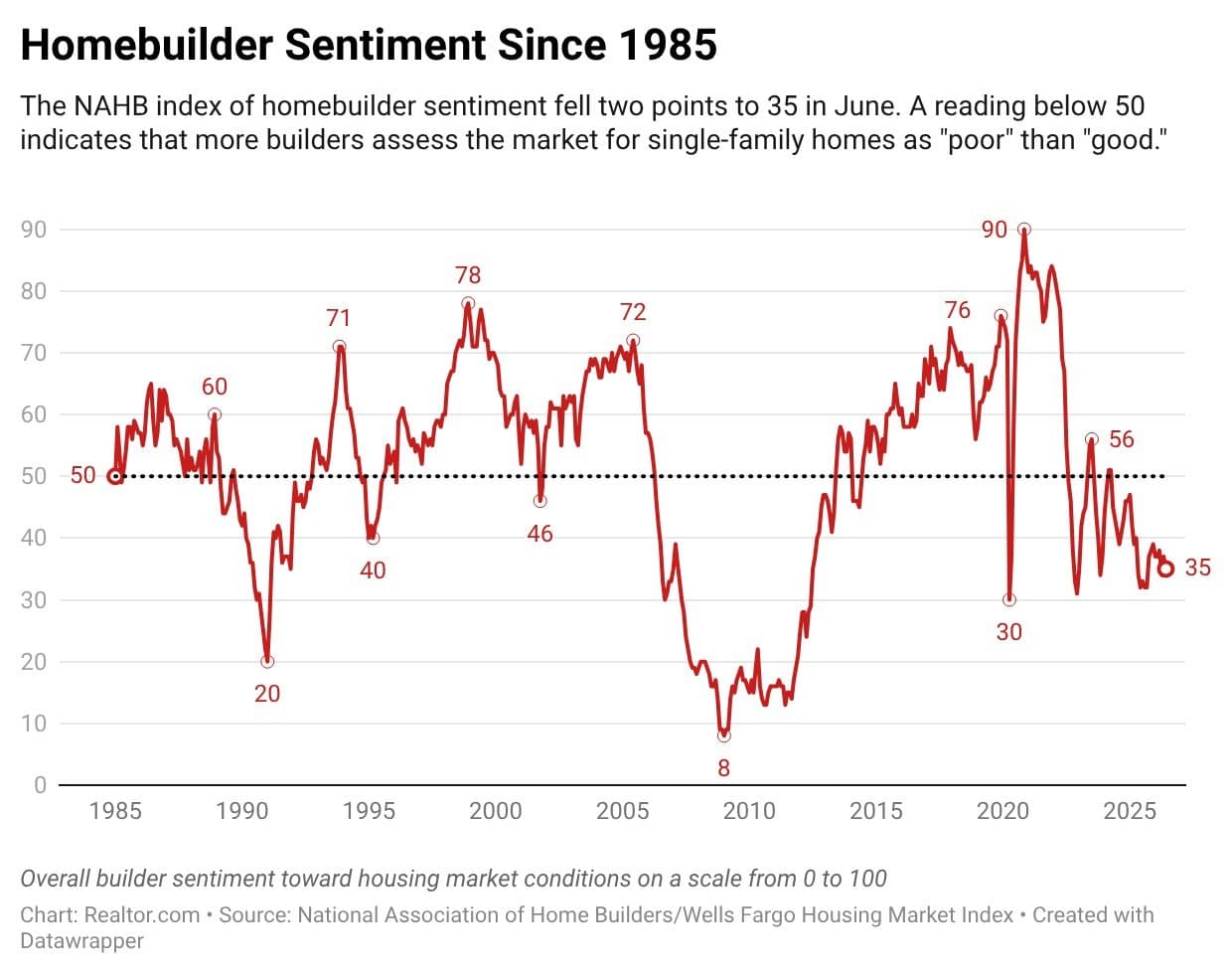

According to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) released this week, builder confidence in the market for newly built single-family homes registered at 35 in June — down from 37 in May. The latest reading signals that pessimism continues to dominate the new construction landscape, with the industry now recording its 14th consecutive month of sentiment below the critical threshold of 40.

What the NAHB Housing Market Index Measures

The NAHB/Wells Fargo Housing Market Index is one of the most closely watched barometers of the U.S. housing industry's health. Each month, the index surveys homebuilders on current sales conditions, buyer traffic, and sales expectations for the next six months, producing a composite score on a scale of 0 to 100.

A reading at or above 50 signals that more builders view conditions as favorable than unfavorable. Conversely, any score below 50 reflects negative sentiment about the market. At 35, June's reading lands firmly in pessimistic territory — and the sustained streak below 40 is a benchmark not seen since the foreclosure crisis of 2011 and 2012, a period that dramatically reshaped the American housing market.

A 14-Month Streak That Echoes the Foreclosure Crisis

The depth and duration of the current builder pessimism cannot be understated. Fourteen consecutive months with sentiment readings below 40 places today's housing construction environment in rare and troubling company. The last time builders endured a comparable stretch of sustained low confidence was during the height of the post-recession foreclosure crisis — a period marked by mass defaults, plummeting home values, and widespread industry contraction.

While today's environment is structurally different — driven more by high borrowing costs and supply-side constraints than by foreclosures — the parallels are difficult to ignore. For prospective homebuyers, real estate professionals, and policymakers alike, this prolonged slump carries significant implications for housing supply, pricing, and long-term affordability.

The Triple Threat Squeezing Builders Right Now

So what exactly is pushing builder confidence to these historic lows? Three interconnected forces are primarily to blame:

- Elevated Mortgage Rates: Mortgage rates have remained stubbornly high throughout 2026, keeping monthly payments out of reach for a large portion of potential buyers. When consumer demand softens, builders pull back on new projects, reducing starts and slowing inventory replenishment. High rates don't just affect buyers — they affect builder financing costs as well, squeezing margins on both sides of the equation.

- Rising Material Costs: Construction materials have continued to rise in price, driven by ongoing supply chain vulnerabilities, tariff pressures, and strong demand from infrastructure and commercial projects competing for the same resources. Lumber, concrete, steel, and labor-intensive components have all seen price increases that eat directly into builder profitability.

- Persistent Affordability Headwinds: The combination of high home prices and elevated borrowing costs has pushed homeownership affordability to generational lows for many Americans. Builders targeting the entry-level and first-time buyer segments — typically the highest-volume end of the market — are finding it increasingly difficult to deliver homes at price points buyers can qualify for.

Industry Leaders Call for Congressional Action

NAHB Chairman Bill Owens was direct in his assessment of what needs to happen next. "With the nation short about 1.2 million homes, builder sentiment will remain soft until barriers are eased and conditions improve for home building," Owens said in the report. "Congress can help by passing the major housing package now before the Senate, along with the CONSTRUCTS Act to address the construction labor shortage and the Energy Choice Act to prevent state and local bans on natural gas in new homes."

Owens' comments highlight the multidimensional nature of the housing supply crisis. It is not simply a matter of demand or financing — structural legislative and regulatory barriers are actively hampering the industry's ability to build at scale. The construction labor shortage, in particular, has been a persistent bottleneck, with the industry struggling to attract and retain enough skilled tradespeople to meet even current reduced levels of demand.

What This Means for the Housing Market and Buyers

For consumers hoping that new construction might help ease the nation's inventory crunch, the prolonged dip in builder confidence is unwelcome news. New home construction represents a critical pipeline for housing supply, particularly in markets where existing homeowners — locked into low mortgage rates from prior years — are reluctant to sell.

When builders lack confidence, they break ground on fewer homes. Fewer new homes mean tighter inventory, which in turn sustains elevated prices and intensifies competition for available listings. This cycle is self-reinforcing: high prices and rates suppress demand, which reduces builder confidence, which limits supply, which keeps prices elevated.

Regional Variations and Market Nuances

It is worth noting that while the national headline number paints a bleak picture, conditions vary meaningfully by region. Some Sun Belt markets with stronger job growth and relatively more affordable land have fared better than coastal metros where regulatory hurdles and land costs compound the broader challenges. Buyers and investors should pay close attention to local market dynamics rather than relying solely on national sentiment readings.

The Road Ahead for Homebuilders

The path to recovery for homebuilder confidence runs through several key variables: a meaningful decline in mortgage rates, stabilization of material costs, legislative relief on labor and regulatory burdens, and a gradual rebuilding of consumer demand. None of these shifts are likely to happen overnight, but even incremental progress on one or more fronts could provide the kind of relief the industry needs to begin turning the tide.

As Congress debates housing-related legislation and the Federal Reserve navigates its monetary policy posture, the construction industry — and the millions of Americans waiting for affordable homes — will be watching closely. Until conditions meaningfully improve, June's reading of 35 serves as a stark reminder of just how fragile the new home construction market remains heading into the second half of 2026.