The Great Wealth Transfer Is Coming—Just Not When It Matters Most

An estimated $124 trillion is expected to change hands across generations by 2048. On paper, this sounds like the financial windfall that could redefine economic mobility for millennials and Gen Z. But beneath the staggering headline number lies a sobering reality: for the vast majority of those who stand to inherit, the money will arrive far too late to make the difference it could have made.

By 2048, even the youngest millennials—those born in 1996—will be 52 years old. The oldest members of the generation will be approaching 67, the traditional age of retirement. What was once framed as a transformative generational opportunity increasingly looks like a retirement cushion arriving at the finish line, rather than a head start at the beginning of the race.

Why Timing Is Everything in Wealth Building

Wealth accumulation is not simply about the amount of money you receive—it is profoundly shaped by when you receive it. Financial decisions made in your 20s and 30s have a compounding effect that can echo for decades. The inverse is equally true: delayed access to capital means delayed entry into wealth-building vehicles, and the compounding losses that follow can never be fully recovered.

Research from Realtor.com makes this point with striking clarity. Buying a first home by age 30 can result in a net worth that is 22.5% higher by age 50 compared to someone who waits just a decade longer to purchase. That is not a marginal difference—it is a structural advantage built on years of equity accumulation, mortgage paydown, and property appreciation. By the time most millennials receive their inheritance, that window has already closed entirely. Even the youngest members of Gen Z will have aged out of this compounding advantage long before 2048 arrives.

"An early transfer doesn't pay one dividend; it changes which financial decisions a family is even able to make for the rest of their lives," said Barry E. Janay, principal and owner of The Law Office of Barry E. Janay. His words capture something that balance sheets alone cannot: early capital does not just solve immediate problems, it reconfigures the entire landscape of future possibility.

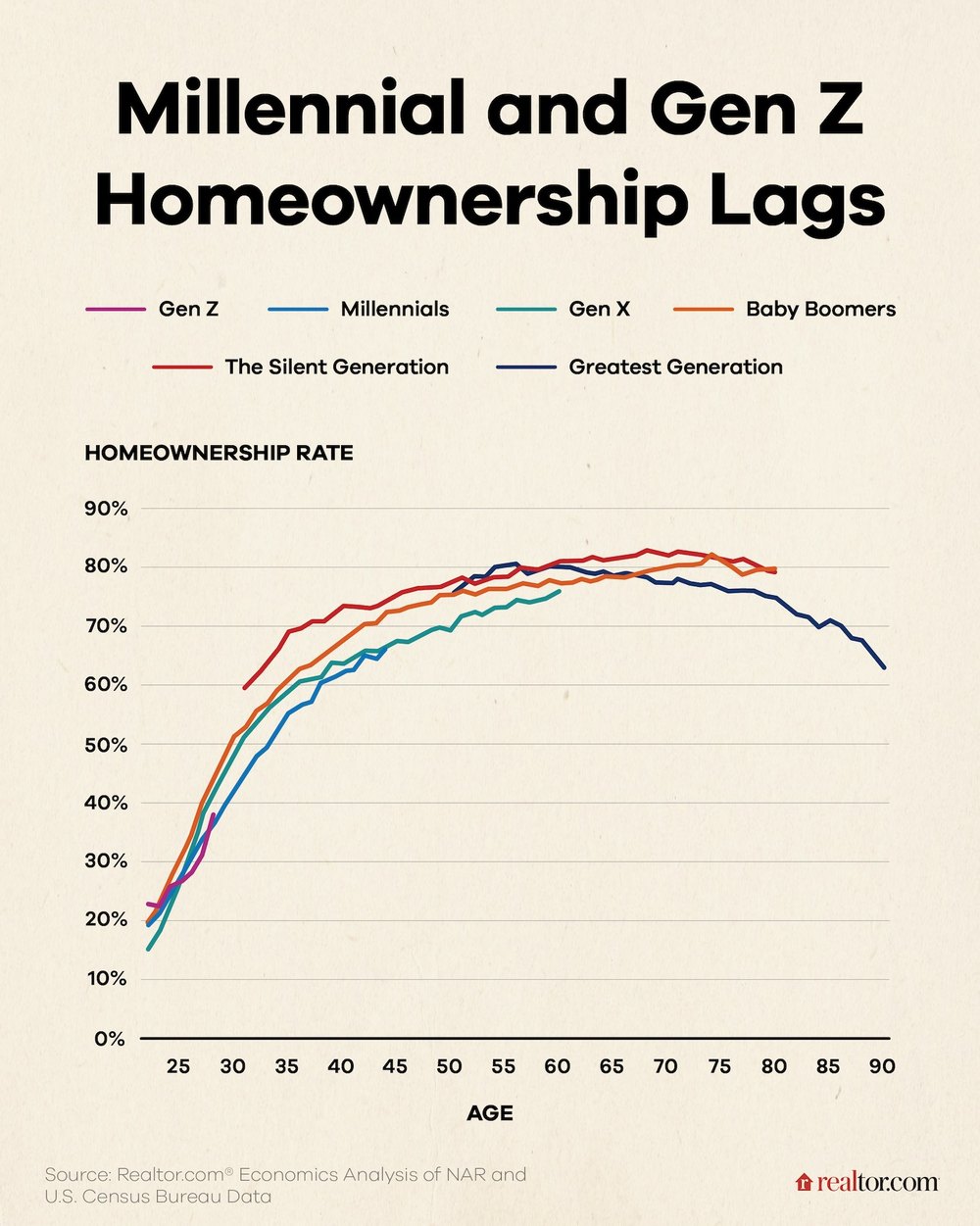

The Hidden Divide: Who Gets Help Early

While the broader wealth transfer remains decades away for most, a quieter, more immediate form of intergenerational support is already underway—and it is shaping the economic outcomes of those lucky enough to access it.

A recent survey found that 59% of parents have provided or plan to provide financial assistance to their children. This help comes in various forms: down payment contributions, outright cash gifts, and coverage of closing costs on home purchases. These transfers may not make headlines the way trillion-dollar inheritance figures do, but their impact on individual financial trajectories is arguably far greater.

For a young adult in their mid-to-late 20s, a $30,000 gift toward a home down payment is not just money—it is a key that unlocks equity, stability, and a generational foothold in the property market. In high-cost metropolitan areas where entry-level homes routinely exceed $400,000 or $500,000, that kind of early family support is often the single deciding factor between homeownership and indefinite renting.

A Tale of Two Millennials

The Great Wealth Transfer is not creating one millennial story—it is creating two. On one side are those who already have access to family capital: they buy homes earlier, carry less debt, have more flexibility in their career choices, and can take entrepreneurial risks that others cannot afford. On the other side are the millions of millennials who will wait for an inheritance that arrives at 52 or 67, spending the intervening decades renting, carrying student debt, and watching the compounding wealth gap widen.

This divide is one of the most consequential in today's economy. It does not merely reflect existing inequality—it actively deepens it. Families with means are finding ways to deploy capital early and strategically, while others are left to navigate the same high-cost environment without that support. The result is not just an income gap but a net worth chasm that grows more difficult to bridge with every passing year.

What Families Can Do Right Now

For families who have the capacity to act, the research makes a compelling case for earlier rather than later transfers. Here is what proactive wealth transfer can look like in practice:

- Down payment gifts: Helping a child purchase a home in their 20s or early 30s can generate decades of equity accumulation and dramatically increase their long-term net worth.

- Annual gift tax exclusions: In the United States, individuals can gift up to $18,000 per year per recipient (as of 2024) without triggering gift tax obligations, making consistent early transfers both legal and tax-efficient.

- Educational funding: Paying down student loans or funding education directly reduces the debt burden that delays wealth-building for millions of younger adults.

- Business seed capital: Early investment in a child's business or professional development can yield returns—both financial and personal—that far exceed traditional inheritance timing.

- Estate planning consultations: Working with an estate attorney early allows families to structure transfers in ways that maximize benefit and minimize tax exposure.

Rethinking the Inheritance Playbook

The traditional model of inheritance—wealth passed down after death, received in middle age or later—is increasingly at odds with the realities of a high-cost, slow-mobility economy. Home prices have surged. Student debt burdens are at historic levels. Wages, adjusted for inflation, have stagnated for working-class and middle-class families. In this environment, leaving a large inheritance at 65 is generous—but leaving a meaningful gift at 28 can be life-altering.

Financial advisors and estate planning professionals are beginning to counsel clients on what some are calling "giving while living"—a philosophy that prioritizes early, strategic transfers over the traditional posthumous distribution of assets. The logic is straightforward: a dollar given to a 28-year-old to buy a home has more compounding potential than the same dollar received at 60, regardless of how large the total estate eventually grows.

The Bottom Line

The Great Wealth Transfer is real, and it will reshape the financial landscape of the United States over the coming decades. But for most millennials and Gen Zers, the timing of that transfer fundamentally limits its transformative potential. The data is clear: early access to capital changes lives in ways that late-stage inheritance simply cannot replicate.

The families, policymakers, and financial professionals who understand this distinction will be the ones best positioned to build genuine, lasting generational wealth—not just the appearance of it. For everyone else, the trillions may arrive right on schedule, and still come far too late.