Mortgage Rates Edge Up to 6.52%: What Homebuyers Need to Know Right Now

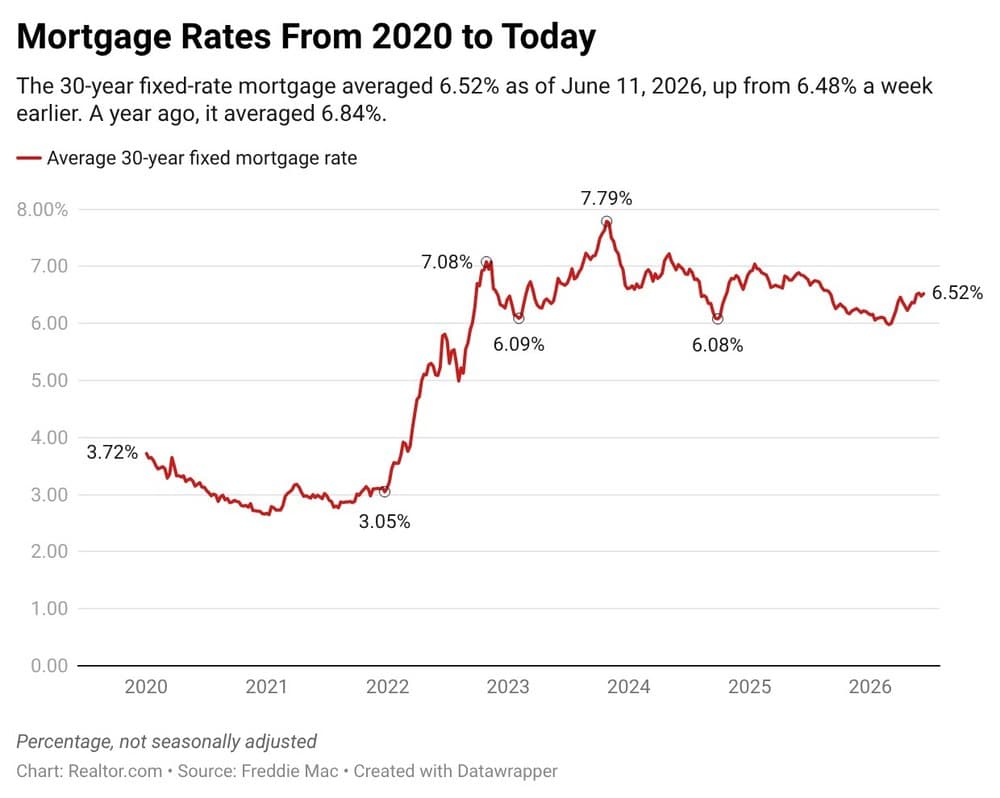

If you've been tracking the housing market lately, you already know that even small shifts in mortgage rates can have a meaningful impact on your monthly budget. This week, the average rate on a 30-year fixed home loan climbed to 6.52% for the week ending June 11, 2026, according to Freddie Mac. That's a modest 4-basis-point increase from the previous week's 6.48%, but when you're borrowing hundreds of thousands of dollars, every fraction of a percentage point matters.

At the same time, the national median home price has risen to $429,500 — a figure that defines the financial reality for the typical American homebuyer today. Together, these two data points shape what homeownership actually costs on a month-to-month basis. So let's break it all down using a mortgage calculator, so you know exactly what to expect before you make one of the biggest financial decisions of your life.

How Today's Rate Compares to Last Year

Before diving into the numbers, it's worth putting the current rate in context. One year ago, in June 2025, the average 30-year fixed mortgage rate stood at 6.84%. That's a full 32 basis points higher than where rates sit today. While 6.52% is not the ultra-low environment buyers enjoyed during the pandemic era, it does represent a measurable improvement over last year's conditions.

For a homebuyer purchasing a median-priced home, that difference translates into real dollar savings every single month — savings that can add up significantly over the life of a 30-year loan. It's a useful reminder that even in a high-rate environment, timing and rate comparisons still matter when making your home purchase decision.

Monthly Mortgage Payment With a 20% Down Payment

The most commonly cited down payment benchmark in homebuying advice is 20%, and for good reason. Putting 20% down eliminates the need for private mortgage insurance (PMI), reduces your loan balance, and generally results in more favorable loan terms. Here's what the numbers look like for today's median-priced home.

On a home priced at $429,500, a 20% down payment comes out to $85,900, leaving a loan amount of $343,600. At the current rate of 6.52%, the monthly principal and interest payment works out to approximately $2,176 per month.

That's $9 more per month than last week's payment of $2,167 — a minor increase driven by the slight rate uptick. More importantly, compare that to June 2025, when the 6.84% rate would have produced a monthly payment of $2,249 on a similarly priced home. Today's buyers are saving roughly $73 per month, or $876 per year, compared to buyers who locked in a year ago at higher rates.

Over the full 30-year term of the loan, that $73 monthly difference amounts to more than $26,000 in savings — a compelling reason not to overlook how much rates have improved, even if they still feel elevated by historical standards.

Monthly Mortgage Payment With a 3.5% Down Payment

Of course, not every buyer has nearly $86,000 sitting in savings for a down payment. Many first-time buyers and those using FHA loans opt for a much lower down payment — often as little as 3.5%. This path to homeownership is more accessible upfront but comes with higher monthly payments due to the larger loan balance, and typically requires mortgage insurance premiums.

On a $429,500 home, a 3.5% down payment equals $15,033, resulting in a loan amount of $414,468. At 6.52%, the monthly principal and interest payment rises to approximately $2,628 per month — roughly $452 more per month than the 20% down scenario.

Again, comparing to June 2025's 6.84% rate, buyers putting 3.5% down are also seeing meaningful monthly relief. The difference in payment between today's rate and last year's translates to real money staying in your pocket each month, helping to offset the ongoing costs of homeownership.

What These Numbers Don't Include

It's important to understand that the figures above reflect only the principal and interest portions of a mortgage payment. Your actual monthly housing costs will be higher once you factor in the following:

- Property taxes: These vary widely by location and can add hundreds of dollars to your monthly payment.

- Homeowners insurance: Required by virtually all lenders, typically ranging from $100 to $200 or more per month depending on your property and region.

- Private mortgage insurance (PMI): Required for conventional loans with less than 20% down, usually costing between 0.5% and 1.5% of the loan amount annually.

- HOA fees: If you're purchasing a condo or a home in a managed community, monthly association dues can add a significant cost.

When budgeting for homeownership, always use a full mortgage calculator that incorporates all of these costs, not just principal and interest, to get a realistic picture of your total monthly obligation.

Tips for Navigating Today's Mortgage Market

Whether you're a first-time buyer or moving up to a larger home, a few strategic moves can help you manage costs in today's rate environment.

- Shop multiple lenders: Rates vary from lender to lender, and even a 0.10% to 0.25% difference can save thousands over the life of your loan.

- Consider your down payment options: If you can increase your down payment, even modestly, you'll reduce your loan balance and potentially avoid PMI.

- Lock your rate when ready: Rate locks typically last 30 to 60 days. If you find a rate you're comfortable with, locking it in protects you from further increases while your purchase closes.

- Improve your credit score: Borrowers with higher credit scores qualify for better rates. Even a small improvement before applying can reduce your monthly payment.

- Use a mortgage calculator: Running the numbers for different scenarios — varying down payments, loan terms, and rates — gives you a clearer sense of what you can realistically afford.

The Bottom Line

At 6.52%, mortgage rates remain elevated compared to the historic lows of recent years, but they represent a genuine improvement over where things stood just 12 months ago. For buyers eyeing the median-priced home at $429,500, the monthly payment with 20% down comes in at approximately $2,176 — affordable for some, a stretch for others, and always dependent on your full financial picture.

The best thing you can do right now is use the tools available to you, run your own numbers, talk to a qualified mortgage lender, and go into the process with a clear-eyed understanding of what homeownership will actually cost you each month. The market is moving, but so is your opportunity to find the right home at the right payment for your budget.