Mortgage Rates Dip to 6.47%: What It Means for Homebuyers This Summer

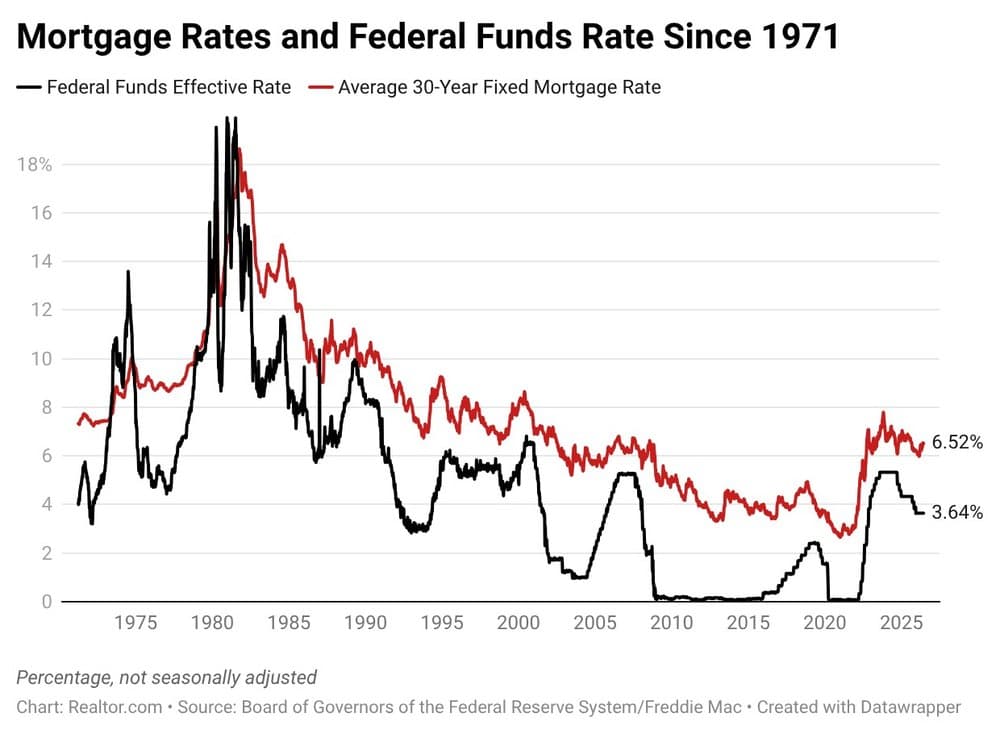

If you've been watching mortgage rates closely, this week brought a small but meaningful piece of good news. According to Freddie Mac, the average rate on a 30-year fixed mortgage fell to 6.47% for the week ending June 18, 2026 — a 5 basis-point drop from the previous week's 6.52%. While that may sound like a minor shift, for buyers navigating today's competitive summer housing market, every fraction of a percentage point adds up to real dollars saved each month.

Even more encouraging, current rates are meaningfully lower than where they stood during the same period in 2025, when the average 30-year fixed rate hovered around 6.81%. That 34 basis-point difference between now and a year ago translates into significant monthly savings for anyone purchasing a home at today's median price.

To give you a clear picture of what these numbers mean at the closing table and beyond, we used the Realtor.com® mortgage calculator to break down the monthly costs for a home priced around the national median of $429,500. All payment examples below are based on a 30-year fixed mortgage and reflect principal and interest only — they do not include property taxes, homeowners insurance, or private mortgage insurance (PMI).

Monthly Payment with a 20% Down Payment

For buyers who can put down the traditional 20%, here is how the math looks today:

- Home price: $429,500

- Down payment (20%): $85,900

- Loan amount: $343,600

- Interest rate: 6.47%

- Monthly principal and interest payment: approximately $2,165

Compared to last week's rate of 6.52%, which produced a monthly payment of $2,176, this week's rate saves buyers about $11 per month. That may seem modest in isolation, but over a 12-month period, that amounts to $132 back in your pocket — and over the life of a 30-year loan, the cumulative savings grow considerably.

The year-over-year comparison is even more striking. At June 2025's average rate of 6.81%, the same $343,600 loan would have cost approximately $2,242 per month. Today's buyers are saving $77 every single month compared to borrowers who locked in a rate a year ago. That is $924 in annual savings, or more than $27,000 saved over the full 30-year term of the loan.

Monthly Payment with a 3.5% Down Payment (FHA Loan)

Not every buyer has 20% saved and ready to go. For many first-time homebuyers and those with limited savings, an FHA loan with a minimum 3.5% down payment is a more realistic path to homeownership. Here is how that scenario plays out at today's rate:

- Home price: $429,500

- Down payment (3.5%): $15,033

- Loan amount: $414,468

- Interest rate: 6.47%

- Monthly principal and interest payment: approximately $2,613

While the lower down payment makes it easier to get into a home sooner, borrowers should be aware that FHA loans come with mortgage insurance premiums (MIP), which will add to the total monthly payment. Still, the drop in rates from last year's levels helps offset some of that additional cost, making FHA loans a more attractive option right now than they were throughout much of 2025.

Why This Rate Drop Matters in a Competitive Summer Market

Summer has traditionally been one of the busiest seasons in real estate, and 2026 is proving to be no exception. Inventory remains tight in many markets across the country, and buyer competition continues to push offers close to — and sometimes above — asking price. In this environment, even a small decrease in mortgage rates can provide meaningful relief by lowering your monthly payment and improving your overall purchasing power.

When rates fall, buyers can afford slightly more home without increasing their monthly budget, or they can keep their target price the same and enjoy lower payments. Either way, this week's rate dip is a window of opportunity worth taking seriously if you have been sitting on the sidelines waiting for conditions to improve.

How to Use a Mortgage Calculator to Plan Your Purchase

One of the smartest steps any prospective homebuyer can take before starting their search is spending time with a mortgage calculator. Tools like the one available on Realtor.com® allow you to input variables such as home price, down payment, interest rate, and loan term to get an instant estimate of your potential monthly payment.

Here are a few tips for getting the most accurate and useful results from a mortgage calculator:

- Include all costs: Remember that your real monthly payment will include property taxes, homeowners insurance, and possibly PMI or MIP. Add these to your calculator estimate for a fuller picture.

- Run multiple scenarios: Try different down payment amounts, home prices, and interest rates to understand how each variable affects your payment and overall affordability.

- Factor in your debt-to-income ratio: Lenders typically want your total monthly debt obligations — including your mortgage — to stay below 43% of your gross monthly income. Use this benchmark to stay within a realistic budget.

- Check rates frequently: Mortgage rates can change week to week, and even small movements have a tangible impact on what you can afford. Stay current and get pre-approved when rates are favorable.

Is Now a Good Time to Buy a Home?

Whether now is the right time to buy depends on your personal financial situation, local market conditions, and long-term goals. However, from a rate perspective, today's environment is more favorable than it was a year ago. At 6.47%, rates are still elevated by historical standards, but the downward trend from the highs of 2023 and 2024 provides cautious optimism for buyers who are ready and financially prepared.

If you have been building your savings, improving your credit score, and researching neighborhoods, this week's dip in mortgage rates is an encouraging signal. Getting pre-approved now can lock in a competitive rate and put you in a strong position when you find the right home.

Bottom Line

Mortgage rates dropping to 6.47% this week offers a tangible benefit for homebuyers targeting a home in the $430,000 range. Whether you plan to put down 20% or are exploring FHA loan options with 3.5% down, the savings compared to last year's rates are real and meaningful. Use a mortgage calculator to model your own scenario, speak with a licensed mortgage professional, and take advantage of this week's more favorable lending environment while it lasts.