Mortgage Rates Climb to 6.52% as Inflation and Jobs Data Rattle Markets

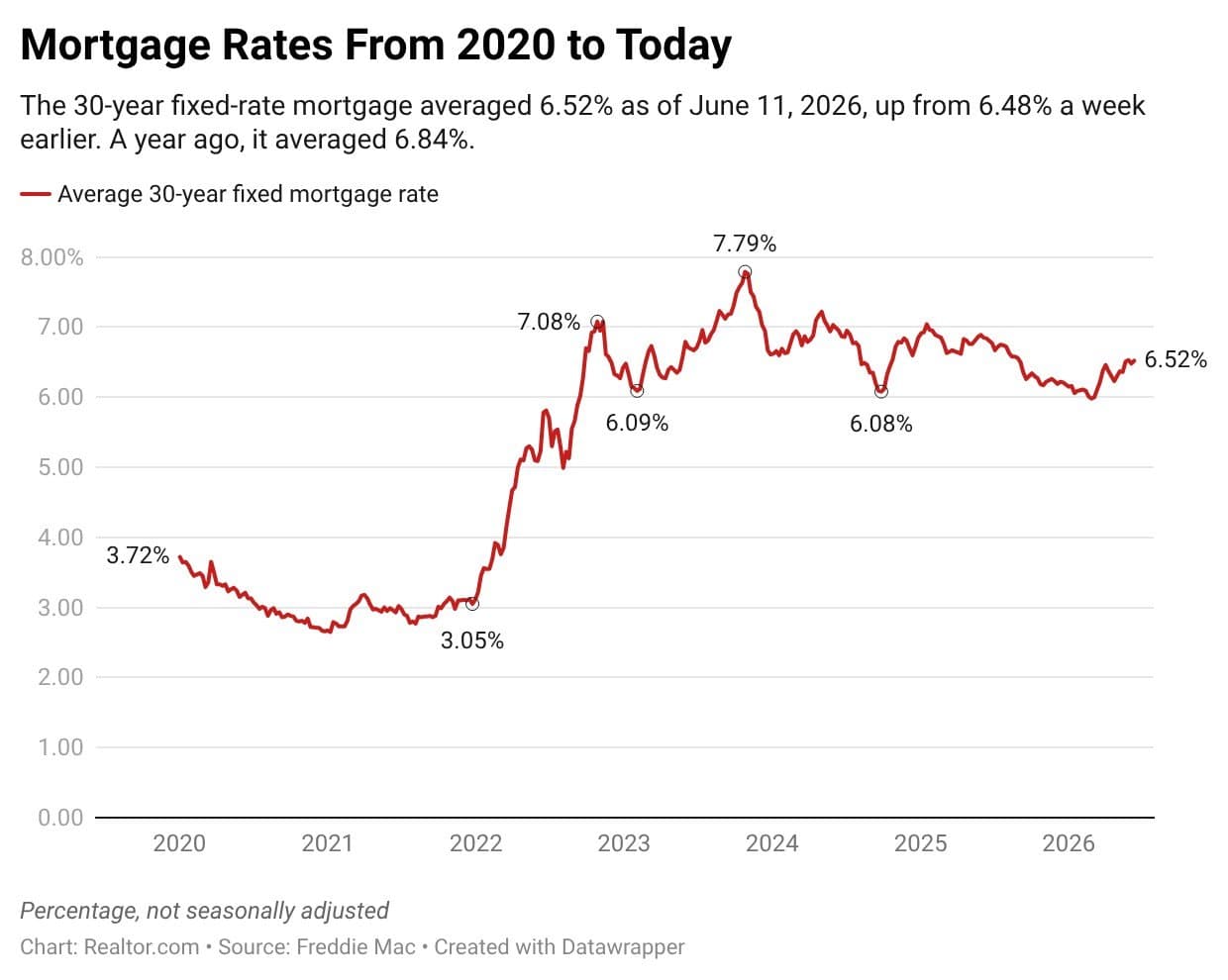

Homebuyers navigating an already competitive housing market received fresh news this week: the average rate on a 30-year fixed mortgage rose to 6.52% for the week ending June 11, 2026, up 4 basis points from 6.48% the prior week, according to data released by Freddie Mac. The uptick follows a stronger-than-expected jobs report and a surge in inflation to a three-year high—a combination that has all but extinguished hopes for a Federal Reserve interest rate cut anytime soon.

Despite the headwinds, real estate professionals and economists are pointing to a more encouraging subplot: buyers are not retreating. In fact, existing home sales have climbed to a five-month high, suggesting that consumer confidence in homeownership remains resilient even as borrowing costs hold steady at elevated levels.

What's Driving the Rate Increase?

Two major economic reports released this week sent mortgage rates higher and reshaped expectations for monetary policy through the rest of the year.

A Jobs Market That Refuses to Cool

The U.S. economy added 172,000 new jobs in May, surpassing early forecasts and reinforcing the narrative of a labor market that continues to outperform expectations. The unemployment rate held steady at 4.3% for the third consecutive month—a streak that signals broad economic resilience rather than a one-time anomaly. While strong employment data is generally positive news for American households, it creates a complex situation for mortgage borrowers. A robust labor market reduces the urgency for the Federal Reserve to cut its benchmark interest rate, which in turn keeps mortgage rates elevated.

Inflation Hits a Three-Year High

Compounding the situation, inflation rose to its highest level in three years, further dimming the prospects for near-term Fed intervention. The Federal Reserve has maintained that it will not reduce interest rates until it sees clear and sustained evidence that inflation is moving back toward its 2% target. With consumer prices climbing rather than falling, that threshold appears further away than many had hoped entering 2026. Investors, who had previously priced in one or two rate cuts before year's end, have been forced to reassess those expectations dramatically.

How Does 6.52% Compare Historically?

Context matters enormously when evaluating mortgage rates. While 6.52% may feel discouraging compared to the sub-3% rates that defined the pandemic-era housing boom of 2020 and 2021, it is worth noting that the current rate represents a meaningful improvement from where things stood just one year ago. During the same week in 2025, the 30-year fixed-rate mortgage averaged 6.84%—a full 32 basis points higher than today's reading. For a borrower taking out a $400,000 loan, that difference translates to a savings of roughly $85 per month, or more than $1,000 annually.

Viewed through a longer historical lens, rates in the mid-6% range remain broadly in line with long-run averages that preceded the extraordinary low-rate environment of the 2010s and early 2020s. Many housing economists argue that buyers who anchored their expectations to those historically anomalous rates may need to recalibrate their thinking about what constitutes a "normal" borrowing environment.

Buyers Are Pushing Forward Anyway

Perhaps the most striking takeaway from this week's data is not the rate increase itself, but the response—or rather the non-response—from potential homebuyers. Sam Khater, Freddie Mac's chief economist, struck a notably optimistic tone in his assessment of the data.

"The 30-year fixed-rate mortgage averaged 6.52% this week," Khater noted. "Stronger employment momentum has helped existing home sales reach a five-month high. Importantly, we're seeing homebuyers look past the short-term rate fluctuations and actively enter the market, signaling renewed confidence in homeownership opportunities."

This behavioral shift is significant. After a prolonged period of rate-driven hesitation that froze transaction volumes across much of 2023 and 2024, buyers appear to be recalibrating their expectations and moving forward with purchases. Several factors may be driving this renewed activity.

Why Buyers Aren't Waiting on the Sidelines

- Rate fatigue: After years of waiting for rates to fall dramatically, many buyers have concluded that meaningful cuts may not materialize in the near term. Rather than continue deferring homeownership, they are choosing to act now and refinance later if conditions improve.

- Job security: A strong labor market means more buyers feel financially confident enough to commit to a 30-year mortgage. Stable employment is one of the most powerful motivators for major financial decisions like purchasing a home.

- Inventory dynamics: While housing supply has improved modestly compared to the extreme scarcity of prior years, desirable properties in sought-after markets still move quickly. Buyers who wait risk losing out to competing offers.

- Home price trends: In many markets, home prices have proven more durable than expected. Some buyers are entering the market now to avoid potentially higher prices down the road, even if they must accept today's borrowing costs.

What This Means for the Fed's Next Move

The Federal Reserve's next policy meeting will be watched closely by mortgage market participants. With inflation running hot and employment robust, the central bank has little political or economic cover to justify a rate reduction in the immediate future. Most economists now project that any Fed rate cut is unlikely before late 2026 at the earliest, and some have pushed their forecasts into 2027.

It is important for buyers to understand that the Fed does not directly set mortgage rates. Rather, 30-year fixed mortgage rates are more closely tied to the yield on 10-year U.S. Treasury bonds, which themselves respond to inflation expectations, economic data, and investor sentiment. Even if the Fed eventually cuts its benchmark rate, mortgage rates could remain stubbornly elevated if inflation and growth expectations stay firm.

Practical Advice for Today's Homebuyers

Navigating a 6.52% rate environment requires a strategic and clear-eyed approach. Here are a few considerations for buyers who are active in the market right now.

- Shop multiple lenders: Rates can vary meaningfully from one lender to another. Getting quotes from at least three to five lenders—including banks, credit unions, and online mortgage companies—can help you secure a more competitive offer.

- Consider points: Paying mortgage discount points upfront to buy down your interest rate can make sense if you plan to stay in your home for several years. Run the math carefully to determine your break-even timeline.

- Lock your rate wisely: In a volatile rate environment, locking your rate as soon as you have a purchase contract can protect you from sudden upward moves. Speak with your lender about float-down options that allow you to benefit if rates dip before closing.

- Focus on total affordability: Rather than fixating solely on the interest rate, evaluate the full picture of your monthly payment, including property taxes, insurance, and HOA fees, alongside your household budget and long-term financial goals.

The Bottom Line

Mortgage rates rising to 6.52% is undeniably a challenge for affordability, particularly for first-time buyers stretching to enter the market. But the data tells a story of resilience rather than retreat. With existing home sales hitting a five-month high and buyers demonstrating renewed confidence despite rate pressures, the housing market appears to be finding its footing in a higher-for-longer rate world. For those who have been waiting on the sidelines for a dramatic rate reversal, the current environment may be as good an entry point as any—especially with rates still tracking below where they were just one year ago.

Staying informed, working with experienced mortgage professionals, and making decisions based on your individual financial situation—rather than broader market noise—remains the most reliable path forward for prospective homeowners in 2026.