Mortgage Rates Climb to 6.49% as Economic Uncertainty Persists

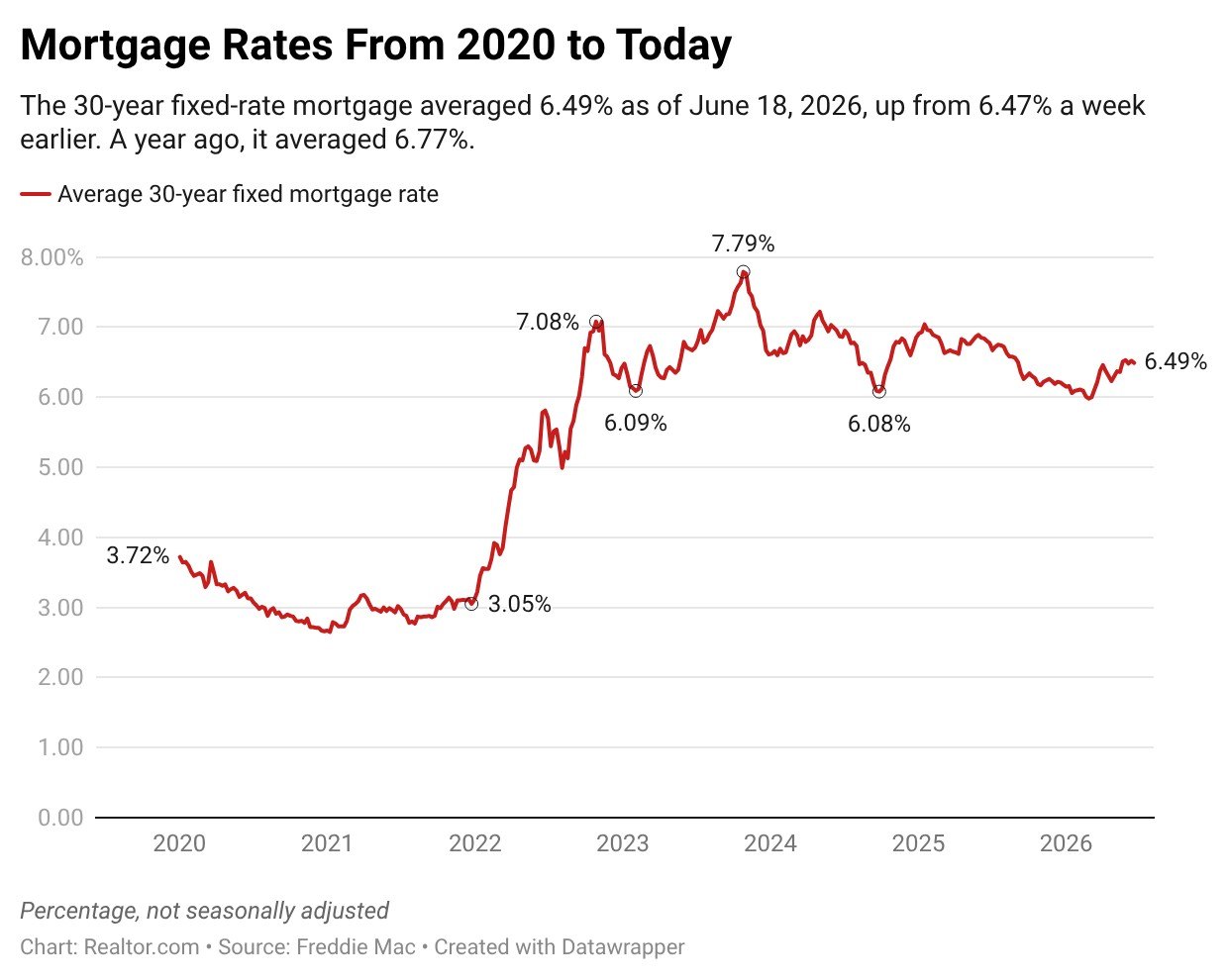

Homebuyers hoping for relief at the closing table got disappointing news this week. Mortgage rates ticked upward to 6.49% for the week ending June 25, 2026, rising 2 basis points from the previous week's 6.47%, according to data released by Freddie Mac. The modest but telling increase signals that even major geopolitical developments — including the recently signed U.S.-Iran peace agreement and the sharp drop in oil prices that followed — have not been enough to meaningfully reduce the economic uncertainty weighing on the housing market.

For many buyers and homeowners watching rate movements, this is the new reality: a mortgage market that stubbornly hovers near 6.5%, showing little appetite to move significantly lower in either direction. Understanding what is driving this stability — and what it means for your buying power — is more important than ever.

Six Consecutive Weeks Near 6.5%: Stability or Stagnation?

Thursday's mortgage reading marks the sixth consecutive week that the 30-year fixed rate has remained in the vicinity of 6.5%. That kind of consistency might sound reassuring on the surface, but financial experts are careful to distinguish between stability and improvement. Rates are stable, yes — but they remain elevated by historical post-pandemic standards, and they show no strong signs of trending downward.

Sam Khater, Freddie Mac's chief economist, put it plainly: "The average 30-year fixed mortgage rate was little changed this week at 6.49%. Rates have remained relatively stable over the last six weeks. Meanwhile, purchase activity eased modestly and refinance activity has continued to pick up recently, reflecting borrowers' responsiveness to current rate levels."

That uptick in refinance activity is a meaningful data point. It suggests that a segment of homeowners who locked in rates at even higher levels during the peak of the rate-hike cycle — some above 7% or 7.5% — are now finding it worthwhile to refinance into today's rates. However, for prospective buyers still sitting on the sidelines waiting for a dramatic rate drop, the data offers little immediate comfort.

Why Didn't the Iran Deal Push Rates Lower?

One of the more striking takeaways from this week's data is the disconnect between global events and mortgage rate movement. On Wednesday, crude oil prices plunged 4% following the announcement of the U.S.-Iran peace agreement, a development that markets had widely interpreted as a potential catalyst for broader economic relief. The ripple effect sent 10-year Treasury yields down more than 8 basis points, dropping to 4.406%.

Under normal circumstances, a significant drop in Treasury yields — which serve as a key benchmark for mortgage rates — would be expected to pull home loan rates lower in kind. But that transmission failed to materialize. Mortgage rates edged up instead, underscoring just how many competing forces are at play in today's rate environment.

Analysts point to a range of factors that can decouple mortgage rates from Treasury movements, including lender profit margins, investor demand for mortgage-backed securities, and broader credit market conditions. When uncertainty remains elevated across multiple dimensions of the economy — from trade policy and fiscal concerns to inflation expectations — lenders tend to price that risk into mortgage rates regardless of short-term Treasury movements.

Comparing 2026 Rates to Last Year: Some Progress, But Far From the Finish Line

To put this week's rate in perspective, it helps to look back at where rates stood during the same period in 2025. For the comparable week one year ago, the 30-year fixed mortgage rate averaged 6.77%. That means buyers today are borrowing at rates roughly 28 basis points lower than they were 12 months ago — a modest but real improvement that translates into hundreds of dollars in savings over the life of a loan.

On a $400,000 mortgage, for example, the difference between a 6.77% and a 6.49% rate amounts to approximately $75 less per month in principal and interest payments. Multiplied over 30 years, that gap adds up to around $27,000 in total interest savings — not a figure to ignore, even if it doesn't quite feel like the relief buyers were hoping for.

What This Means for Homebuyers in Today's Market

If you are actively shopping for a home or preparing to enter the market, the current rate environment calls for a recalibrated strategy. Here are key considerations to keep in mind:

- Adjust your budget expectations now. With rates anchored near 6.5%, it is wise to run your purchase numbers at this rate rather than waiting for a meaningful drop that may not come soon. Basing affordability calculations on 5% or lower rates could leave you financially stretched if conditions don't change.

- Lock in when rates dip, even briefly. Rate fluctuations of even a few basis points can create short windows of opportunity. Work with your lender to understand your lock options and be ready to move when conditions are favorable.

- Consider shorter loan terms or adjustable-rate products carefully. Some buyers are exploring 15-year fixed loans or adjustable-rate mortgages (ARMs) to access lower initial rates. These products carry their own risks and rewards and should be weighed thoughtfully based on your timeline and financial situation.

- Don't wait indefinitely. Market timing is notoriously difficult. Home prices in many areas continue to hold steady or appreciate, meaning that delaying a purchase in hopes of lower rates could cost you in home price appreciation even if borrowing costs improve.

Purchase Activity Eases While Refinancing Gains Momentum

The divergence between purchase activity and refinance demand tells an important story about where the market currently stands. Purchase applications pulled back modestly this week, a sign that affordability pressures continue to keep some buyers on the sidelines. Tight inventory in many markets compounds this challenge, as buyers compete for a limited number of available homes even as demand is somewhat restrained by borrowing costs.

On the refinance side, the trend is more encouraging. Homeowners who purchased or refinanced at peak rates of 7% or higher now have an incentive to revisit their loan terms, and many are acting on it. This uptick in refinance volume is a positive signal for the broader housing market, as it frees up cash flow for existing homeowners and can stimulate consumer spending more broadly.

The Road Ahead: Will Mortgage Rates Fall in the Second Half of 2026?

The central question on every buyer's mind is whether rates will drop meaningfully in the months ahead. The honest answer is that the outlook remains uncertain. Much will depend on incoming inflation data, Federal Reserve policy signals, and broader economic performance. If inflation continues its gradual cooling trend and the Fed moves toward rate cuts, mortgage rates could drift lower toward the 6% range by late 2026. However, persistent fiscal concerns or renewed geopolitical tensions could keep upward pressure on yields and, by extension, home loan rates.

What is clear is that the era of sub-3% or even sub-5% mortgage rates is not returning anytime soon. For buyers and real estate professionals alike, building a strategy around the current rate environment — rather than waiting for a return to previous lows — is the pragmatic and financially sound approach. Welcome to the new normal.