Home Flipping Profits Are Finally Moving in the Right Direction

After nearly two years of painful declines, house flippers across the United States finally have something to celebrate. A new quarterly report from real estate data analytics firm ATTOM reveals that profit margins on flipped homes climbed in the first quarter of 2026, snapping a streak of seven consecutive quarters of losses. While the gain is modest, industry experts say the shift in direction matters far more than the size of the move.

For real estate investors who have been grinding through one of the most challenging flipping environments in over a decade, this data point could mark the beginning of a meaningful recovery — or at least a long-awaited stabilization.

What the Numbers Actually Say

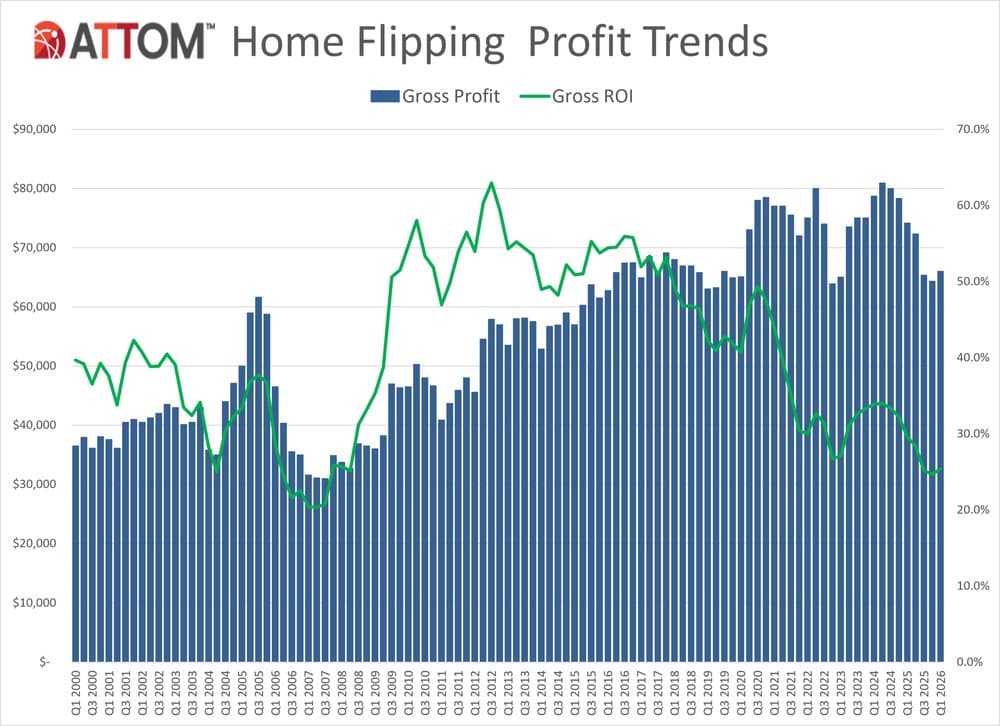

According to ATTOM's Q1 2026 Home Flipping Report, the typical profit margin for a flipped home reached 25.4% in the first quarter of the year, up from 24.7% in the fourth quarter of 2025. That previous reading had been the lowest profit margin recorded since 2008, making the rebound all the more significant from a historical perspective.

To put that in broader context, the last time flippers saw a quarter-over-quarter increase in returns was in early 2024, when the typical national return on investment sat at around 35%. Since then, margins had been in steady freefall, squeezed from both sides by stubbornly high home prices and elevated mortgage interest rates that dampened buyer demand and made it harder to sell flipped properties at a meaningful premium.

The less-than-one-percentage-point gain may look small on paper, but what it signals to the market is substantial: conditions may finally be stabilizing after a prolonged and difficult period for fix-and-flip investors.

Why Flipping Has Been So Tough Recently

To understand why this uptick matters, it helps to understand the dual pressures that have been crushing flipping margins over the past two years. The first is the persistently high cost of acquiring properties. As median home sale prices peaked in 2025, the cost basis for flippers rose sharply, leaving less room to generate profit on the back end of a deal.

The second pressure has been elevated interest rates, which have had a compounding negative effect on the flipping business model in two important ways:

- Higher carrying costs: Flippers who rely on short-term financing to fund acquisitions and renovations have faced significantly higher borrowing costs, eating directly into their net returns on every deal.

- Weakened buyer demand: High mortgage rates have priced many would-be buyers out of the market or pushed them to the sidelines, reducing the pool of end buyers willing to purchase a renovated home at the price needed to generate a healthy profit margin.

- Compressed resale premiums: When buyers are stretched thin and shopping cautiously, they are less willing to pay a significant premium over neighborhood comparables, squeezing the spread between what a flipper pays to acquire and renovate a home and what they can ultimately sell it for.

Together, these forces created what many in the industry described as a "double whammy" — a phrase that aptly captures just how difficult the operating environment became for investors over the past several quarters.

What Industry Leaders Are Saying

ATTOM CEO Rob Barber offered cautious optimism in response to the Q1 2026 data. "The first increase in flipping returns in nearly two years is a welcome sign for investors," Barber said in a prepared statement. "The market remains far more competitive than it was during the peak profit years, but this quarter's gains suggest that conditions may be stabilizing."

Importantly, Barber also flagged that the recovery is unlikely to be uniform across the country. "Success still depends heavily on local market dynamics, with some metros producing strong returns while others remain difficult places to flip profitably," he noted.

That geographic variability is a critical reminder for investors: national averages tell part of the story, but the real opportunities — and real risks — are hyperlocal. A market-by-market approach to deal evaluation remains essential, even as the broader trend starts to improve.

Local Market Dynamics Still Drive Everything

Even in a recovering environment, not all markets are created equal. Some metropolitan areas are seeing strong flipping returns driven by tight housing inventory, robust job markets, and resilient buyer demand. Others continue to struggle, particularly in markets where home prices remain elevated relative to local incomes or where new construction has increased the supply of move-in-ready alternatives to flipped homes.

Savvy investors are paying close attention to metrics like days on market for renovated homes, the spread between distressed and retail pricing in a given zip code, and the pace at which local inventory is moving. These on-the-ground indicators often tell a more accurate story than national averages alone.

What This Means for Real Estate Investors Going Forward

The Q1 2026 data offers a cautiously encouraging signal for anyone involved in or considering entry into the fix-and-flip space. Here are the key takeaways worth keeping in mind:

- The trend has reversed, but the environment is still competitive. A 25.4% profit margin is a far cry from the peak years when returns regularly exceeded 40% to 50% in many markets. Investors should calibrate their expectations accordingly and build conservative assumptions into their underwriting.

- Seven quarters of decline ending matters psychologically and practically. Stabilization can attract capital back into a sector that has seen many investors step back, which may gradually increase deal flow and market activity.

- Interest rate movement will remain a key variable. Any meaningful decline in mortgage rates could meaningfully accelerate the recovery in flipping margins by improving buyer affordability and expanding the pool of qualified end buyers.

- Local expertise is more valuable than ever. As Barber emphasized, national trends mask significant regional variation. Investors with deep knowledge of specific markets will continue to have a distinct advantage.

The Bottom Line

House flipping has been through a genuinely difficult stretch over the past two years, hammered by high acquisition costs and a rate environment that made profitability a real challenge for all but the most disciplined operators. The Q1 2026 data from ATTOM is a meaningful first step toward recovery — not a signal to throw caution to the wind, but a legitimate reason for measured optimism.

For investors who have stayed active and sharpened their processes through the downturn, the improving margin environment could reward patience. For those waiting on the sidelines, now may be the time to start paying close attention again. The tide, it seems, may finally be turning.