America's Housing Crisis Has Two Faces — And One Root Cause

By 2034, the number of Americans aged 65 and older will outnumber children under 18 for the first time in U.S. history. It's a demographic milestone that will ripple across Social Security, healthcare, and nearly every public system the country relies on. But one of its most overlooked consequences is playing out right now in neighborhoods across the nation — in the form of a deepening housing gap that is simultaneously trapping older homeowners in place and shutting younger generations out of the market entirely.

On the surface, these appear to be two separate problems. For younger Americans, skyrocketing home prices and limited inventory have made homeownership feel increasingly out of reach. For older Americans, the challenge looks different — many are staying in homes that no longer suit their needs because there's simply nowhere better to go. But housing experts argue these are not separate crises. They are two symptoms of the same underlying disease: a chronic and worsening shortage of the right kind of housing in the right kinds of places.

The Numbers Behind the Crisis

The U.S. housing shortage is currently estimated at approximately 4.03 million units, according to recent analysis from Realtor.com. That staggering deficit isn't just a matter of not enough homes being built — it's a mismatch between the types of housing that exist and the types that people across different life stages actually need.

Nearly one in three older households is considered cost burdened by their home, meaning they spend a disproportionate share of their income on housing costs. Many of these homeowners would prefer to downsize or move to a more manageable property, but the options available to them are limited, particularly in the communities they've lived in for decades. Without viable places to move, they stay put — and the larger family homes they occupy never become available for younger families who need them.

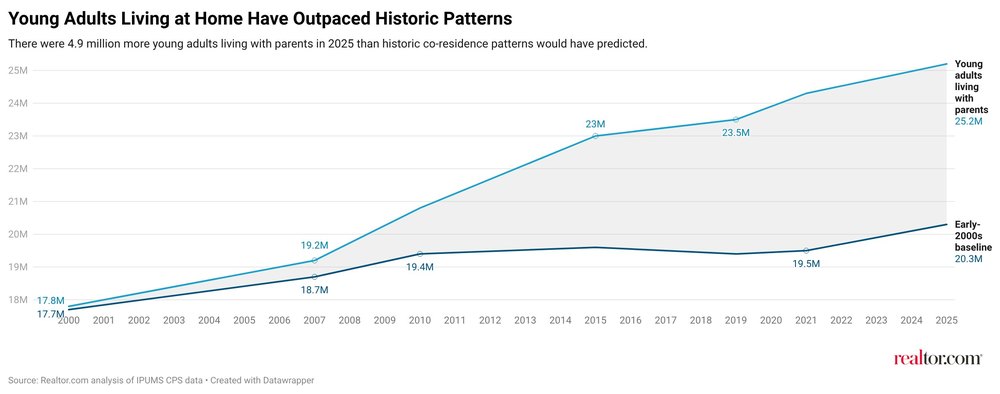

Meanwhile, young adults are spending longer periods living in their parents' homes than any previous generation. High purchase prices, elevated mortgage rates, and fierce competition for what little inventory exists have delayed the path into homeownership for millions of Americans in their 20s and 30s. The dream of owning a first home has not disappeared — but for many, it has been pushed further and further into the future.

A Life Cycle Problem Hiding Inside the Supply Gap

Rodney Harrell, vice president of family, home, and community at AARP's Public Policy Institute, argues that baked into America's housing shortage is a life cycle problem that rarely gets discussed in those terms.

"The big enemy here is a lack of the kind of housing supply that we need, the range of options, particularly in those locations that work for folks," Harrell explains. "People's housing needs change as they age, form families, become caregivers, face health changes, lose income, or decide they no longer want to maintain a large home. Yet many neighborhoods offer only one kind of place to live."

This insight reframes the conversation significantly. The housing crisis is not simply about volume — it's about variety. A neighborhood filled exclusively with large single-family homes may serve a certain life stage well, but it fails older residents who want to downsize within the community they love, and it fails younger buyers who cannot yet afford those larger properties. When the housing ladder has missing rungs, everyone gets stuck.

What Kinds of Housing Are Missing?

Addressing the life cycle gap means expanding the range of housing options available in more communities. Experts and housing advocates frequently point to several underbuilt categories that could help unlock the market for both older and younger Americans:

- Accessory Dwelling Units (ADUs): Smaller secondary units on existing properties can give older homeowners a way to age in place while generating rental income, or provide an affordable entry point for younger renters and buyers.

- Smaller single-family homes: The average size of newly built homes in America has grown significantly over the decades, pricing out buyers who want something modest and manageable. A return to building more starter homes could open doors for first-time buyers.

- Mixed-income and mixed-type developments: Communities that blend condos, townhomes, apartments, and single-family homes allow residents to move through different life stages without relocating far from the neighborhoods, services, and social ties they've built over time.

- Senior-friendly housing near transit and services: Many older Americans want to remain in their communities but need homes that are accessible, lower maintenance, and close to healthcare and transportation — a combination that is chronically underbuilt in most markets.

Why Young Buyers and Older Owners Are Actually Allies

It can be tempting to frame older homeowners and younger buyers as being in competition — occupying the same units, bidding on the same listings. But the more accurate view is that both groups are victims of the same broken system, and both stand to benefit from the same solutions.

When older homeowners have appropriate, desirable options to move into, they can free up the larger homes that growing families need. When younger buyers can access starter homes or smaller units at realistic price points, they begin building equity and eventually move up the housing ladder themselves. That movement creates the natural churn and availability that a healthy housing market depends on. Without diverse supply, the entire system stagnates.

Policy and Community Action Must Catch Up

Closing the housing gap will require more than market forces alone. Zoning laws in many American cities still restrict the types of housing that can be built, effectively enforcing the single-type neighborhood model that leaves so many people without viable options. Reform efforts at the state and local level — including allowing higher-density development, streamlining permitting for ADUs, and incentivizing mixed-use projects — are gaining momentum in some regions but remain slow and politically fraught in others.

Federal investment and policy also play a role, particularly in expanding affordable housing options for cost-burdened older adults and supporting community development in areas that have been historically underbuilt. Social Security pressures, rising healthcare costs, and shifting demographics make housing stability for older Americans not just a quality-of-life issue, but an economic imperative.

The Takeaway: Supply, Variety, and Shared Solutions

The housing gap trapping older owners and shutting out young buyers is not inevitable — it is the result of decades of underbuilding, exclusionary zoning, and a failure to plan for the full arc of how people live. As the U.S. approaches a historic demographic crossroads, the conversation around housing must evolve beyond simple supply numbers and address the deeper question of what kinds of homes, in what kinds of places, will serve an aging and changing population. The good news is that solving for one group's needs tends to unlock solutions for the other. A housing market with more variety is a market that works better for everyone.