Zillow CPI Shelter Forecast April 2026: Housing Inflation Surprises to the Upside

The April 2026 Consumer Price Index (CPI) release delivered a notable surprise for housing economists and market watchers. According to Zillow's shelter inflation forecast and the Bureau of Labor Statistics data published on May 12, 2026, housing inflation came in hotter than anticipated, pushing overall annual inflation to its highest level since 2023. While the broad trend of moderating shelter costs remains intact, the April report raised important short-term questions about the pace of that slowdown.

For renters, homeowners, policymakers, and anyone tracking the Federal Reserve's next moves, understanding what drove this unexpected shelter print — and whether it signals a lasting reversal or a temporary blip — is essential context heading into the second half of 2026.

What the April 2026 CPI Shelter Data Actually Showed

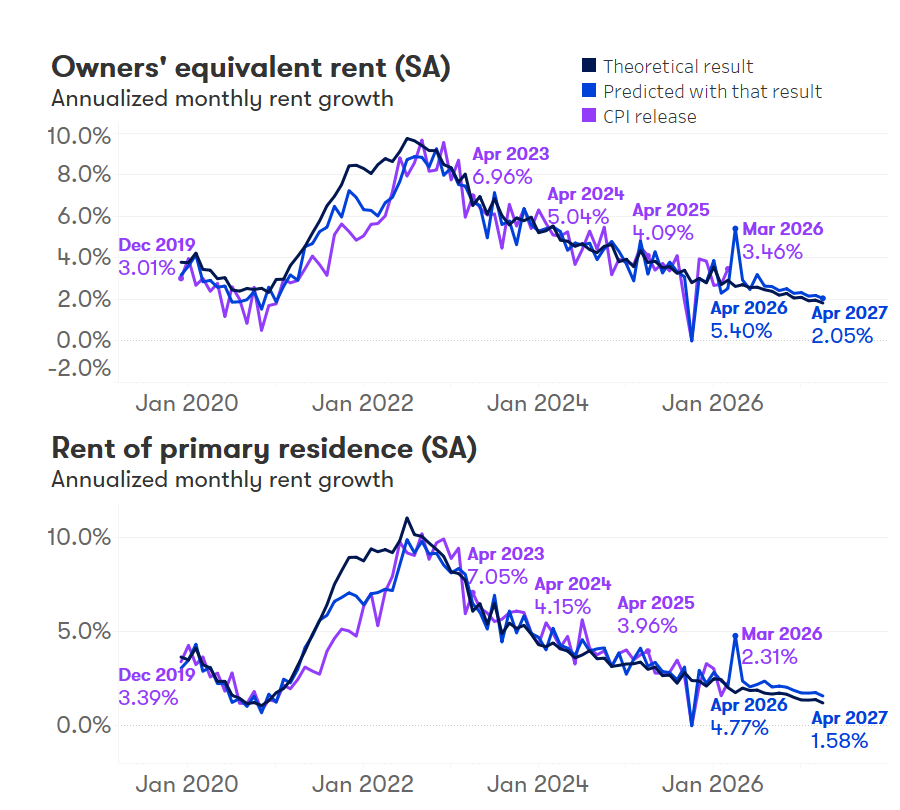

The Bureau of Labor Statistics releases shelter inflation data as part of its monthly CPI report. Within the shelter category, two components carry the most weight: Owner's Equivalent Rent (OER) and Rent of Primary Residence. Both came in above Zillow's pre-release forecasts in April 2026.

Owner's Equivalent Rent (OER)

Seasonally adjusted CPI for Owner's Equivalent Rent increased by 0.53% in April 2026, exceeding Zillow's expectation of 0.44%. On a year-over-year basis, OER rose 3.30%, compared to the 3.20% forecast. OER is one of the single largest components of the entire CPI basket, meaning even modest surprises in this index can have an outsized effect on the headline inflation number.

Rent of Primary Residence

Seasonally adjusted CPI for Rent of Primary Residence rose 0.55% for the month, well above Zillow's expectation of 0.39%. Year-over-year, this measure climbed 2.79%, versus a forecast of 2.63%. This subindex more directly captures what tenants are paying for their apartments and homes, making it a closely watched signal for rental market conditions.

Other Shelter Components

Beyond OER and primary rent, smaller components of the shelter category also contributed to the April surprise. Hotel spending rose 2.8% for the month, and household insurance edged up 0.1%. Taken together, the full shelter category posted a 0.61% increase in April — a notably elevated reading.

Why Did Housing Inflation Come In Hotter Than Expected?

The elevated April print was not entirely unexpected in directional terms. Zillow and other forecasters had anticipated some upside risk related to the government shutdown, which disrupted the regular collection and processing of survey data used to compile the shelter indexes. Statistical artifacts from data collection interruptions can temporarily distort monthly CPI readings, which is why analysts had already adjusted their expectations somewhat.

However, the actual April release exceeded even those adjusted expectations, landing near the upper extreme of Zillow's confidence bands. This raised a genuine analytical question: was the extra heat driven by recent months' economic activity, or should it be interpreted as a carryover effect from methodological and data changes that occurred in 2025? At this point, the answer remains unclear, and Zillow acknowledged the ambiguity directly in its post-release update.

What is clear is that a single elevated monthly print does not necessarily reverse the broader disinflationary trend in housing costs. Shelter inflation is a lagging indicator by nature — the CPI measures what tenants are currently paying under active leases, not what new leases are being signed at in the open market. New market rents have been decelerating for well over a year, and that dynamic feeds into the official CPI indexes with a significant delay.

The Big Picture: Is Housing Inflation Still Slowing Down?

Despite the April surprise, Zillow's underlying estimates continue to show that housing inflation is on a downward trajectory. The primary driver of that deceleration is the cooling in market rents — what landlords are actually advertising for new tenants. As these lower new-lease rents gradually cycle into the mix of leases captured by the CPI survey, they pull the official shelter indexes lower over time.

Zillow's forecast maintains that housing will remain an overall disinflationary force on consumer prices throughout 2026. This is a significant statement, given that shelter carries the largest single weight in the CPI basket. If housing costs continue to moderate on a trend basis, that takes meaningful pressure off the headline inflation numbers that the Federal Reserve monitors when setting interest rate policy.

Key factors supporting the continued moderation forecast include:

- Elevated apartment supply: A construction boom that began during the pandemic has delivered a substantial number of new rental units to markets across the country, giving renters more options and limiting landlords' ability to push rents higher.

- Softening demand in some metros: Certain high-cost cities are seeing population stabilization or even modest outflows, reducing the demand pressure that fueled rapid rent growth in 2021 and 2022.

- Lease renewal dynamics: As pandemic-era leases continue to roll over, fewer tenants are facing the extreme catch-up rent increases that were common in 2022 and 2023.

- Mortgage rate sensitivity: Elevated mortgage rates have continued to suppress home-buying activity, keeping more households in the rental market but also capping the extreme price appreciation that previously fed OER estimates.

What This Means for Renters and Homeowners in 2026

For renters, the April CPI data is a reminder that even as the overall trend points lower, shelter costs are not falling in absolute terms — they are simply rising more slowly. Rent of Primary Residence is still up 2.79% year over year. That is a slower pace than the 5% to 8% annual increases seen during the peak of the pandemic rental surge, but it still represents a real cost increase for household budgets.

For prospective homebuyers, the interplay between CPI shelter data and Federal Reserve policy is particularly important. If elevated shelter prints persist in coming months, they could complicate the Fed's path toward potential interest rate cuts, keeping mortgage rates elevated for longer. Conversely, if the April reading proves to be a one-month anomaly consistent with the government shutdown disruption theory, subsequent releases may revert to the softer trend and support a more favorable rate environment later in 2026.

For homeowners tracking the value of their real estate, a gradual normalization of housing inflation — rather than a sharp correction — is generally the most constructive scenario. It suggests a soft landing for housing markets rather than the kind of rapid price adjustment that would erode equity.

What to Watch in the Coming Months

The May and June 2026 CPI shelter releases will be critical in determining whether April's elevated reading was an outlier or the beginning of a trend reversal. Analysts will be watching OER and Rent of Primary Residence closely for signs that the government shutdown artifact has faded and that the underlying moderation trend has resumed. Zillow's ongoing monthly shelter forecasts will provide a useful benchmark for setting expectations ahead of each release.

In the meantime, the foundational story for 2026 housing inflation remains largely intact: market rents are cooling, new supply is supporting tenants, and the official CPI indexes are expected to gradually reflect those conditions. April's surprise does not change that outlook — but it does underscore that the path lower will not be perfectly smooth.