Capital Gains Tax Is Locking Homeowners in Place — And the Senate Is Paying Attention

If you've ever wondered why so few homes seem to be available for sale in your area, the answer might not be what you expect. While high mortgage rates and new construction shortfalls certainly play a role, a growing body of evidence points to another silent culprit: the federal capital gains tax on home sale profits. In a significant Senate hearing this week, real estate industry leaders made their case that outdated tax thresholds are effectively trapping millions of homeowners — particularly older Americans — in properties they would otherwise be ready to sell.

What Happened at the Senate Hearing?

The Senate Committee on Banking, Housing and Urban Affairs heard testimony Tuesday from Kevin Brown, president of the National Association of Realtors® (NAR). Brown's message was direct: the current capital gains tax exclusion limits for home sellers are badly out of date, and the consequences are rippling through the entire housing market.

Under current federal law, homeowners can exclude up to $250,000 in profits from a home sale if they are single filers, or up to $500,000 if they are married and filing jointly. Any gains above those thresholds are subject to the federal capital gains tax, which can reach rates of 15% or even 20% depending on income level. The problem, according to NAR, is that these limits were set in 1997 and have never been adjusted for inflation — despite the fact that home values in many parts of the country have more than doubled or tripled since then.

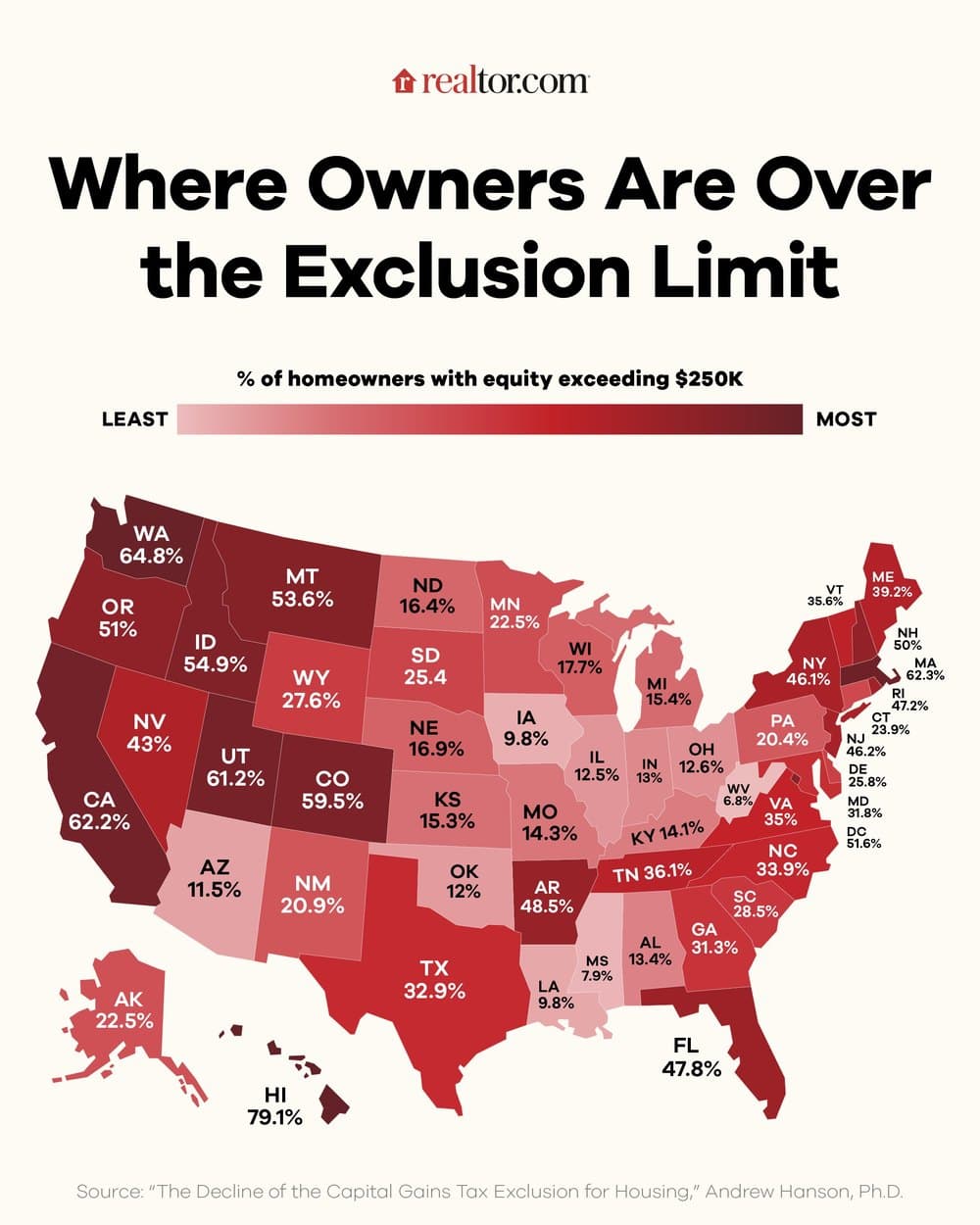

The Numbers Tell a Sobering Story

The math behind NAR's concern is straightforward. A homeowner who purchased a house in a major metropolitan area 20 or 30 years ago for $200,000 may now find that same home worth $800,000 or more. For a single filer, that means roughly $350,000 in taxable gains after applying the $250,000 exclusion. At a capital gains tax rate of 15%, that's a tax bill of more than $52,000 — a significant financial penalty simply for deciding to downsize, relocate, or access equity built up over decades.

This "home equity penalty," as Brown described it during his Senate testimony, hits senior homeowners especially hard. Many retirees have relied on their home equity as a central pillar of their retirement planning. When facing a five-figure tax bill upon selling, the calculus often tips toward staying put rather than moving — even when a smaller, more manageable property would better fit their current lifestyle and needs.

NAR's Proposal: Double the Exclusion Limits

To address this, NAR is urging Congress to double the existing exclusion thresholds. Under the proposed change, single filers would be exempt from capital gains taxes on up to $500,000 in home sale profits, while married couples filing jointly would receive an exclusion of up to $1,000,000. This adjustment would more accurately reflect decades of home price appreciation and give millions of homeowners a genuine financial pathway to sell.

Brown testified that raising these limits would have a measurable and meaningful impact on housing supply. "Just like people were locked into their homes at lower interest rates, seniors are often locked in because of the home equity penalty," he told the committee. "This legislation expands existing housing stock and gives seniors the opportunity to tap equity that they have counted on for retirement."

The ripple effect of unlocking that inventory could be significant. When longtime owners sell, they free up homes for move-up buyers — households looking to transition from a starter home into something larger. Those move-up buyers, in turn, vacate their smaller properties, which then become available for first-time homebuyers. In a market starved for entry-level inventory, this kind of chain reaction could provide meaningful relief without requiring new construction.

A Lock-In Effect With Multiple Causes

The capital gains lock-in effect exists alongside — and compounds — another well-documented phenomenon: the mortgage rate lock-in. Millions of homeowners who refinanced or purchased during the historically low interest rate environment of 2020 and 2021 now carry mortgage rates below 3% or 4%. Selling their home would mean taking on a new mortgage at today's rates, which hover considerably higher, making a move financially painful even for those who want to downsize or relocate.

Taken together, these two lock-in pressures create a significant drag on housing supply. Addressing the capital gains threshold wouldn't solve everything, but it would remove one major barrier that is keeping an identifiable segment of willing sellers — particularly older, long-term homeowners — on the sidelines.

What Would This Mean for First-Time Buyers?

The potential downstream benefits for first-time buyers are one of the most compelling arguments in favor of reform. Inventory of entry-level homes remains critically low in most U.S. markets. If tax reform encourages seniors and long-term homeowners to list their properties, it could release a meaningful wave of existing homes into markets that desperately need them.

First-time buyers who have been priced out or simply unable to find available homes may find more options emerge if the capital gains exclusion is updated. While tax reform alone won't solve the affordability crisis, advocates argue it is an important and relatively straightforward policy lever that Congress can pull right now.

What Comes Next?

Following the Senate hearing, the proposal to raise capital gains exclusion limits will continue working through the legislative process. NAR and other housing industry groups are expected to continue pushing for the change as part of broader conversations around housing affordability and supply. Whether Congress ultimately acts remains to be seen, but the Senate hearing signals that lawmakers are at least listening to the argument that the tax code itself may be one of the biggest barriers to a healthier housing market.

For homeowners sitting on significant equity and wondering whether it makes financial sense to sell, the answer right now may genuinely depend on what Washington decides to do next.