Housing Inflation Runs Hotter Than Expected in April 2026

The May 12, 2026 release of the Consumer Price Index brought an unwelcome surprise for economists and policymakers: housing inflation came in above forecasts, pushing overall annual inflation to its highest level since 2023. According to Zillow's CPI Shelter Forecast analysis, both major shelter components — Owner's Equivalent Rent and Rent of Primary Residence — exceeded expectations, raising fresh questions about the pace of disinflation in the U.S. housing market.

While analysts had already braced for an elevated reading partly due to data processing disruptions tied to the government shutdown, the actual numbers landed near the upper extreme of Zillow's confidence bands. That means even the adjusted, more cautious projections were not pessimistic enough to fully account for April's result.

Breaking Down the April 2026 CPI Shelter Numbers

To understand what this report means for everyday Americans, it helps to look closely at the two primary components of shelter inflation tracked by the Bureau of Labor Statistics.

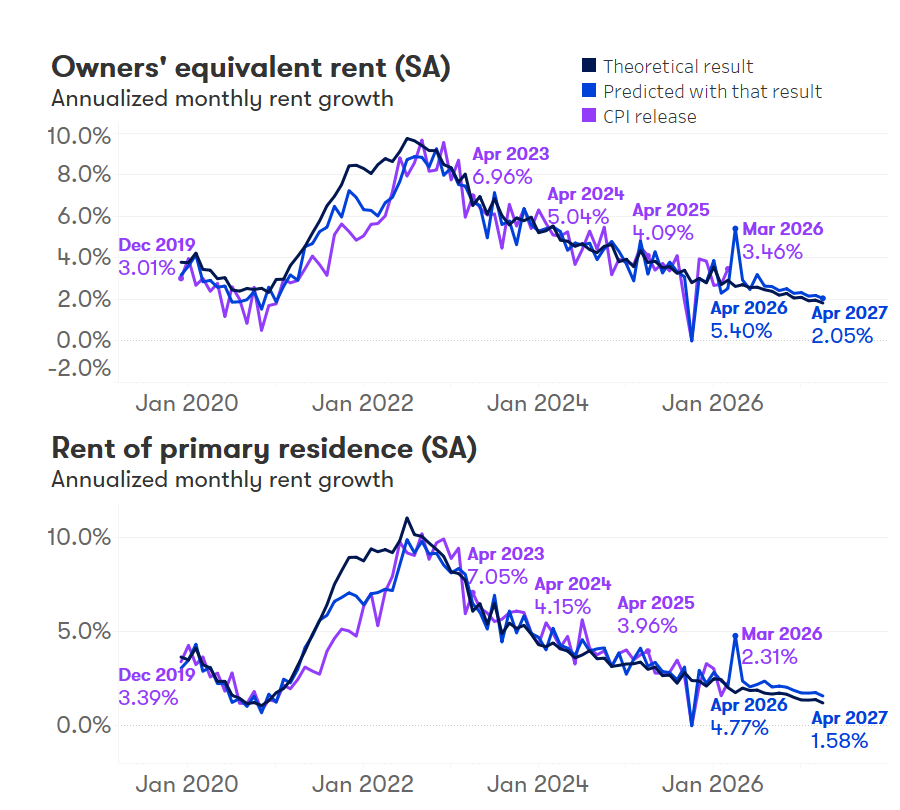

Owner's Equivalent Rent (OER)

Seasonally adjusted CPI for Owner's Equivalent Rent increased by 0.53% in April 2026, surpassing Zillow's forecast of 0.44%. On a year-over-year basis, OER rose 3.30%, compared to the anticipated 3.20%. OER is the largest single component of the CPI basket, representing roughly a quarter of the entire index. Even a modest overshoot in this category can have an outsized effect on the headline inflation number. For homeowners, OER doesn't directly translate to a bill they pay each month — it reflects the hypothetical rent their home would command on the open market — but its weight in the CPI makes it one of the most consequential data points in inflation measurement.

Rent of Primary Residence

Seasonally adjusted CPI for Rent of Primary Residence rose 0.55% in April, considerably above Zillow's expectation of 0.39%. Year over year, this measure climbed 2.79%, versus a forecast of 2.63%. This component captures what actual renters are paying month to month and is closely watched as a real-world barometer of housing affordability. The fact that it came in 16 basis points above the monthly expectation signals that rental markets may still be absorbing more pricing pressure than models predicted.

Other Shelter Sub-Components

Smaller categories within the shelter index also contributed to April's elevated reading. Overall shelter inflation rose 0.61% for the month, with hotel and lodging costs jumping 2.8% and household insurance inching up 0.1%. These figures, while individually modest, pile on top of the OER and rent increases to paint a picture of broad-based shelter price pressure in the spring of 2026.

Why Did Inflation Come in So High? The Government Shutdown Factor

One of the complicating factors in interpreting the April 2026 CPI is the lingering effect of the recent government shutdown. Disruptions to federal data collection can create statistical artifacts — delayed surveys, imputed values, or catch-up adjustments — that temporarily distort official readings. Zillow's analysts had already built a higher baseline into their April forecast to account for this possibility. Nevertheless, the actual print still exceeded that adjusted expectation.

The key unresolved question is whether the extra heat reflects genuine, underlying rent pressure that has been building in recent months, or whether it is largely a statistical carry-over from 2025 data revisions. Zillow's team has not yet reached a firm conclusion, noting that it is "unclear whether the extra heat can be attributed to recent months or should be written off as 2025 changes." The May and June CPI releases will be critical in determining which interpretation is correct.

The Bigger Picture: Is Housing Still a Disinflationary Force in 2026?

Despite April's surprise, Zillow's underlying outlook for housing inflation remains cautiously optimistic. The firm continues to project that shelter inflation will decelerate through the remainder of 2026, primarily driven by a slowdown in market rents. This distinction matters: the CPI shelter components lag real-time market conditions by roughly 12 to 18 months, meaning that the cooling in asking rents already documented in 2024 and 2025 is still working its way into official inflation statistics.

In plain terms, the CPI is still catching up to a rental market that has already begun to soften. As that lag resolves, shelter inflation should exert a downward — or disinflationary — influence on the broader Consumer Price Index for the rest of the year.

What This Means for Renters, Homeowners, and the Fed

For renters, the near-term outlook is mixed. Official CPI rent measures remain elevated, but real-world asking rents in many metro areas have plateaued or even declined from their 2022–2023 peaks. Renters negotiating new leases or renewals in mid-2026 may find more flexibility than the headline CPI numbers suggest.

For homeowners, the OER overshoot does not translate to higher mortgage payments, but it does affect broader financial conditions. Persistently high shelter inflation keeps overall CPI elevated, which can influence Federal Reserve policy decisions on interest rates. If the Fed interprets April's print as evidence of sticky inflation rather than a one-time anomaly, it may delay any planned rate cuts — keeping mortgage rates higher for longer.

- Renters in high-demand metros should monitor local asking rent data alongside the national CPI figures for a more accurate picture of their specific market.

- Homeowners considering refinancing should watch upcoming CPI releases in May and June to gauge whether the Fed's rate posture is likely to shift.

- Investors in residential real estate should note that while CPI shelter remains elevated, the leading indicators from market rent indices point toward continued deceleration in NOI growth.

- First-time buyers remain in a challenging environment where both home prices and borrowing costs are elevated, though any Fed pivot triggered by cooling inflation could improve affordability conditions later in 2026.

What to Watch in the Coming Months

The next several CPI releases will be decisive. If May and June data confirm that April's overshoot was an anomaly tied to the government shutdown adjustment, markets and policymakers can look through it. If, however, subsequent prints also come in above expectations, it would suggest that housing disinflation is progressing more slowly than anticipated — a scenario that could complicate the Fed's path toward rate normalization.

Zillow's forecast model will continue to update as new lease data flows in from its platform, offering one of the most granular real-time views of where rents are heading before those changes reach official statistics. For anyone tracking housing costs — whether as a renter, a buyer, a landlord, or a policymaker — keeping a close eye on both the CPI shelter data and leading market rent indicators remains essential in navigating the 2026 housing landscape.

Final Thoughts

April 2026's CPI shelter report was a reminder that even well-calibrated forecasts can be humbled by noisy data. The overshoot in both Owner's Equivalent Rent and Rent of Primary Residence pushed overall inflation to multi-year highs, but the structural story in housing — slower market rents gradually pulling official measures lower — remains intact. Patience and data vigilance will be the defining traits of sound housing market analysis for the months ahead.