The $124 Trillion Promise That May Arrive Too Late

There is something quietly devastating about the so-called Great Wealth Transfer. Economists and financial planners have spent years talking about it as a generational windfall—trillions of dollars flowing from Baby Boomers and the Silent Generation down to their children and grandchildren. The numbers are staggering. An estimated $124 trillion is projected to change hands between generations through 2048. For millennials, who are positioned to receive a significant share of that transfer, it sounds like a lifeline.

But there is a catch. A significant one. By 2048, the youngest millennials will be 52 years old. The oldest will be approaching 67. And while that timing may be early enough to pad a retirement account or pay off lingering debt, it is almost certainly too late to do what inherited wealth does best: change the entire arc of a person's financial life.

Why Timing Is the Most Underrated Factor in Wealth Building

Wealth is not just about how much money you have. It is about when you have it. Financial decisions made in your 20s and 30s compound over decades in ways that decisions made in your 50s simply cannot replicate. Buying a home, avoiding high-interest debt, funding a business, building an investment portfolio—all of these strategies benefit enormously from time.

Research from Realtor.com makes this point with striking clarity. Buying a first home by age 30 can result in a net worth that is 22.5% higher by age 50 compared to someone who waits just ten years to make that same purchase. The difference is not the house itself—it is the compounding equity, the years of appreciation, and the financial stability that homeownership creates over time. By the time most millennials receive their inheritance, that compounding window will have closed entirely.

"An early transfer doesn't pay one dividend; it changes which financial decisions a family is even able to make for the rest of their lives," says Barry E. Janay, principal and owner of The Law Office of Barry E. Janay. That framing is important. Inheritance is not just money—it is optionality. It is the ability to say yes to opportunities that would otherwise be out of reach.

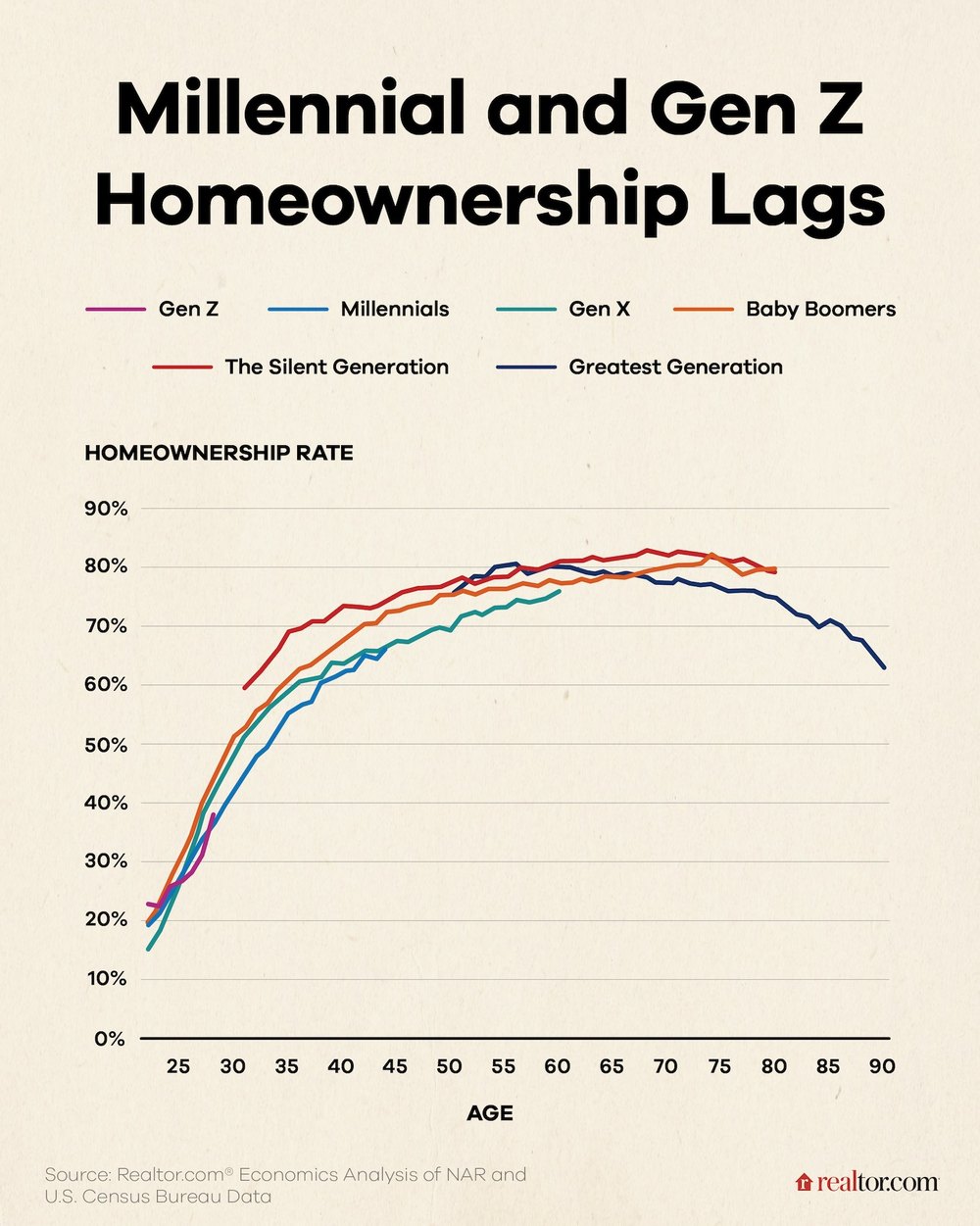

The Homeownership Gap Is Already Widening

For millions of millennials, the dream of homeownership has been deferred not by lack of ambition but by structural economic forces. Student loan debt, stagnant wage growth relative to housing costs, and a real estate market characterized by historically low inventory and high prices have combined to make first-time homeownership extraordinarily difficult without outside help.

This is where the generational wealth divide becomes not just a personal finance story but a social one. Families with the means and the foresight to transfer wealth early—through down payment gifts, co-signing loans, or direct cash contributions—are giving their children a fundamentally different starting point. A recent survey found that 59% of parents have already provided or plan to provide financial assistance to their children for home purchases, including down payment contributions, cash gifts, and help with closing costs.

That number sounds encouraging until you consider what it implies for the other 41%. Those families—often lower-income, often from communities that were historically excluded from wealth-building opportunities—are sending their children into one of the most expensive housing markets in modern history without a safety net. The result is a widening gap not just in wealth but in the foundational stability that wealth enables: stable housing, proximity to good schools, lower financial stress, and the freedom to take career risks.

Early Transfers Are Reshaping Economic Mobility

In an era defined by economic stagnation and rising costs, early family wealth transfers have become one of the most powerful engines of upward mobility—and one of the least discussed. While public conversations about wealth inequality often focus on income, the more decisive factor for many households is access to capital at the right moment.

Consider what a $30,000 gift means to a 28-year-old trying to enter a housing market where the median down payment in major cities can exceed that amount. It is not just a house. It is years of building equity instead of paying rent. It is a credit profile that improves with each on-time mortgage payment. It is the ability to relocate for a better job without the financial fragility of month-to-month renting. It is, in short, a different life.

Now consider that same $30,000 arriving at age 55. It helps. But it does not transform. The compounding years are gone. The homeownership window has largely passed. The career flexibility that capital enables is far more limited late in a working life.

Gen Z Is Already Feeling the Squeeze

Millennials are not the only generation watching this dynamic play out. Gen Z, currently entering the workforce and the housing market, faces an even more compressed timeline. Even the youngest members of Gen Z will be well past the critical early-adulthood wealth-building window by the time the bulk of the Great Wealth Transfer concludes in 2048. Without early family support, many will find themselves locked out of the same compounding advantages their parents never had either.

This creates a self-reinforcing cycle. Families that transferred wealth early produce children who build wealth earlier, who are better positioned to transfer wealth early to their own children. Families that cannot make early transfers—whether due to their own financial constraints or the timing of inheritance—produce children who face the same structural disadvantages, regardless of how large a check eventually arrives.

What Families Can Do Now

The research and expert consensus point in the same direction: if your goal is to meaningfully improve the financial trajectory of your children or grandchildren, earlier is almost always better. There are several strategies families can consider regardless of their overall wealth level.

Down payment assistance: Even modest contributions toward a first home purchase can accelerate homeownership by years and unlock decades of compounding equity.

Early gifting: Under current IRS annual gift tax exclusion rules, individuals can gift a set amount per year per recipient without triggering gift tax, making incremental early transfers a practical option for many families.

Educational and career investment: Covering education costs or helping a young adult avoid student loan debt frees up income that would otherwise go to debt service, accelerating wealth accumulation.

Estate planning conversations: Simply having transparent, early conversations about inheritance plans allows children to make better-informed financial decisions, even before money changes hands.

The Real Lesson of the Great Wealth Transfer

The Great Wealth Transfer is real, and its scale is genuinely historic. But the lesson it teaches is less about the amount of wealth being transferred and more about when it arrives. Trillions of dollars flowing to people in their 50s and 60s will ease retirements and settle estates. That is not nothing. But it will not close the homeownership gap. It will not reverse decades of missed compounding. It will not give back the years when capital could have changed not just a balance sheet but an entire life's direction.

The families who understand this—and act on it early—are quietly writing a different story. The question for policymakers, financial advisors, and families alike is whether that story can be made available to more people, not just those who were lucky enough to have the timing work in their favor.