The Housing Market Is Changing Hands—Literally

For years, headlines about the housing market were dominated by fears of Wall Street gobbling up single-family homes at scale, squeezing out everyday buyers and turning American neighborhoods into corporate rental portfolios. But a notable shift is underway. According to a new investor report from Realtor.com®, small or "mom-and-pop" investors are increasingly calling the shots in the U.S. housing market, while large institutional players are pulling back in a significant way. Add a shifting political landscape to the mix, and 2025 may well mark a turning point in how the American housing market is shaped for years to come.

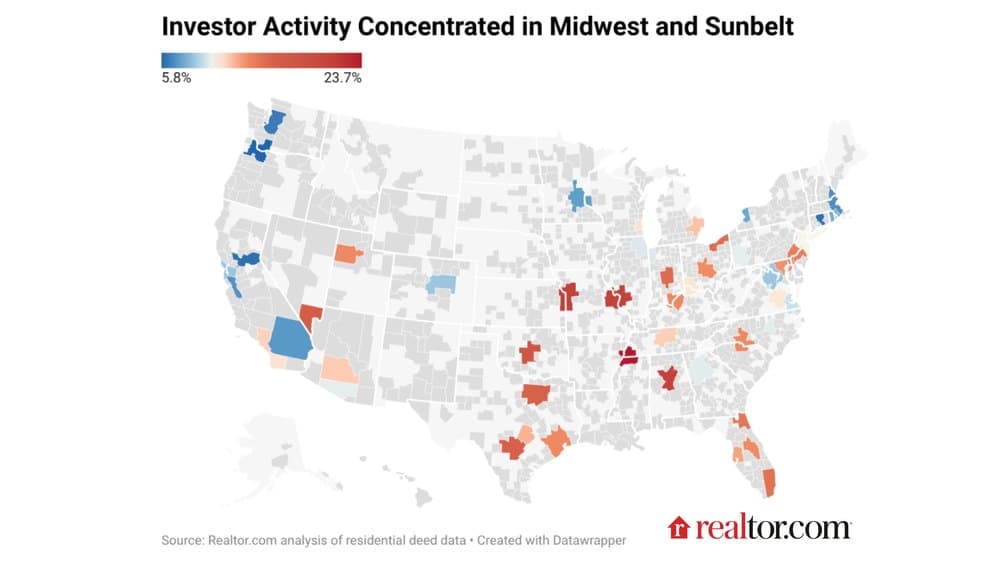

Investor Activity Holds Steady, but the Players Are Changing

Overall investor activity in the housing market ticked up modestly in 2025. Investors accounted for 11.3% of all home sales—up 0.3 percentage points from the previous year. In raw numbers, investors purchased approximately 534,000 homes throughout the year. The median investor purchase price also climbed by 5.6%, a figure that outpaced the broader market's rate of home price appreciation. This narrowing gap between what investors and non-investors pay suggests a tightening competitive dynamic, one where individual buyers and small investors increasingly find themselves on the same playing field.

But beneath the relatively flat headline numbers lies a story of dramatic structural change. Not all investors are created equal, and the data makes clear that large-scale, institutional buyers are rapidly ceding ground to their smaller counterparts.

Small Investors Are the Big Winners

Perhaps the most striking finding from the Realtor.com® report is that small investors now collectively account for two-thirds of all investor-purchased housing stock. These are the mom-and-pop landlords—individuals or small partnerships who own a handful of properties, often as a retirement strategy or a way to build generational wealth. Far from being passive bystanders, these buyers have become the backbone of investment activity in today's housing market.

This rise of the small investor reflects several broader economic trends. As stock market volatility has made equities feel unpredictable for many households, tangible assets like real estate remain an attractive store of value. For many Americans, owning a rental property or two continues to represent a practical and accessible path to financial security—one that doesn't require access to Wall Street capital or complex financial instruments.

Wall Street Is Retreating—and the Numbers Are Stark

On the other end of the spectrum, large institutional investors have experienced a dramatic and sustained pullback from the housing market. Since their peak activity in 2021, large investors have declined by nearly 70%—a staggering contraction that signals a fundamental reassessment of residential real estate as an asset class at scale. Even "mega" investors, defined as entities owning 350 or more homes, have not been immune: that segment has declined by approximately 30% from its 2021 high-water mark.

Several factors are likely driving this retreat. Rising interest rates over the past several years have made leveraged real estate acquisition significantly more expensive, compressing the margins that made large-scale buy-to-rent strategies so attractive in the post-2008 era. Declining rent growth in many markets has further eroded the investment thesis for institutional players who need to deliver consistent returns to shareholders and fund managers.

The Political Climate Adds a New Layer of Pressure

Beyond pure economics, the policy environment in Washington has shifted in ways that carry real consequences for large housing investors. In early 2026, President Donald Trump began publicly scrutinizing the role of large institutional investors in the housing market, directing attention toward whether corporate ownership of single-family homes was contributing to the affordability crisis facing millions of American families.

Congress followed the administration's lead, advancing landmark housing legislation aimed at addressing investor activity and bringing more supply and fairness to the market. While the full effects of this legislation had not yet worked their way into 2025's data, the signal being sent from Washington is clear: large-scale institutional ownership of single-family homes is facing a new era of political and regulatory scrutiny, regardless of party lines.

This legislative momentum—combined with the market-driven retreat already underway—suggests that the era of Wall Street dominating the single-family home market may genuinely be drawing to a close.

What This Means for Everyday Homebuyers

For prospective homebuyers and housing market watchers, the shift away from institutional dominance carries both hopeful and cautionary notes.

- More competition at the entry level: As small investors continue to be active buyers, first-time homebuyers may still face competition—particularly in affordable price tiers where mom-and-pop investors often focus their activity.

- Less bulk purchasing pressure: The dramatic pullback from large investors likely reduces the kind of all-cash, bulk-buying pressure on inventory that was particularly acute between 2020 and 2022.

- Policy tailwinds: Ongoing legislative attention to housing reform may generate additional supply over time, which would benefit buyers across the board—though meaningful supply increases typically take years to materialize.

- Market normalization: The narrowing gap between investor and non-investor purchase prices hints at a market that is gradually normalizing after years of post-pandemic distortions.

A Housing Market in Transition

The 2025 data paints a picture of a housing market in the middle of a genuine transition. The Wall Street-backed institutional land grab that defined much of the early 2020s has clearly lost steam, driven by economic headwinds and growing political opposition. In its place, the market is seeing a return to a more traditionally structured investor landscape—one anchored by individual Americans making calculated bets on real estate rather than institutional asset managers deploying billions in capital.

Whether this transition proves durable will depend heavily on how interest rates evolve, how quickly Congress's legislative efforts translate into tangible market change, and whether the underlying affordability crisis that has defined the housing market for more than a decade can finally begin to ease. For now, the data suggests that the American dream of owning property—whether to live in or to rent out—remains alive and well, and increasingly in the hands of everyday investors rather than corporate giants.

The Bottom Line

Small, individual investors now own a commanding majority of investor-held housing stock, Wall Street buyers are retreating at historic rates, and Washington is paying more attention to housing policy than it has in decades. The convergence of these forces means that the housing market landscape of 2025 looks fundamentally different from just four years ago—and the story is still being written. For anyone watching the real estate market, whether as a buyer, a seller, a renter, or a policymaker, understanding who is actually buying homes has never been more important.