Mortgage Rates Pull Back: What a 6.47% Rate Means for Homebuyers in 2026

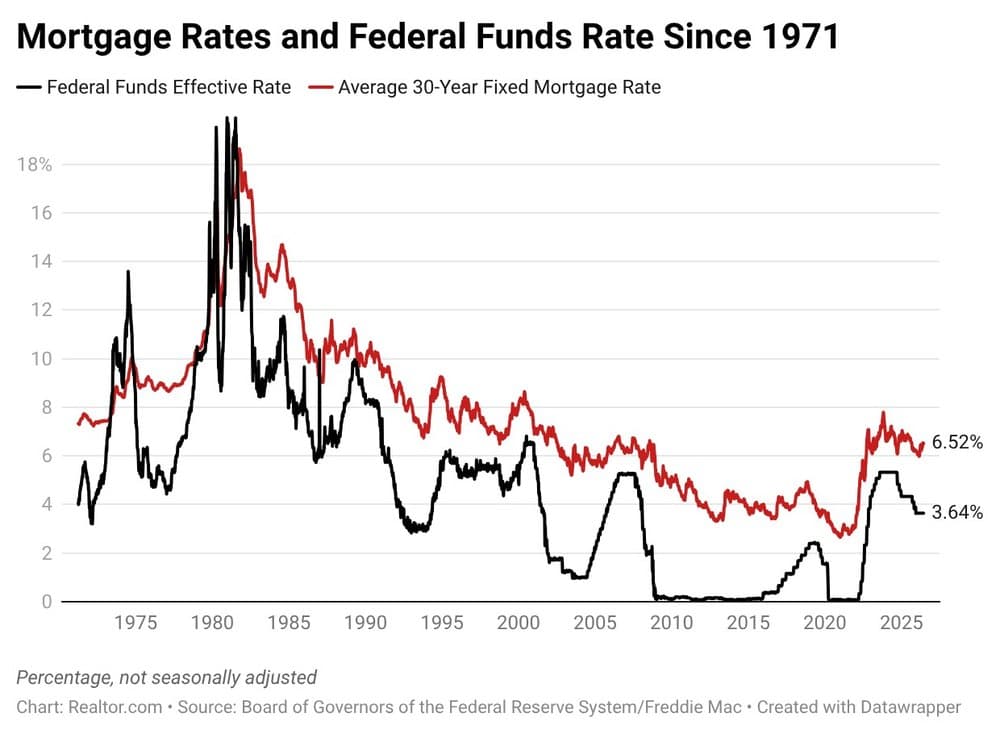

If you've been watching mortgage rates closely, there's some encouraging news to report. For the week ending June 18, 2026, the average rate on a 30-year fixed home loan dropped to 6.47%, according to Freddie Mac. That's down 5 basis points from the previous week's 6.52% and meaningfully lower than the 6.81% average recorded during the same period in 2025. While it may seem like a modest shift, even small rate changes can translate into hundreds of dollars in savings over the life of a loan — and real relief on your monthly budget.

So what does this rate environment actually mean if you're shopping for a home right now? Using a mortgage calculator, we can break down the numbers on a median-priced home to show exactly how the math plays out under today's conditions.

Understanding the Median Home Price

The national median home price currently sits at approximately $429,500. That's the benchmark we'll use throughout this breakdown. It's worth noting that median prices vary significantly by region — a home in rural Tennessee will look very different from one in suburban California — but the $429,500 figure gives us a useful, nationally relevant starting point for understanding how today's rates affect affordability.

All examples below assume a 30-year fixed-rate mortgage and account for principal and interest only. They do not include property taxes, homeowners insurance, or private mortgage insurance (PMI), which can add a meaningful amount to your total monthly housing cost depending on your location and loan type.

Monthly Payment With a 20% Down Payment

For buyers who are able to put down 20%, the math looks like this. On a $429,500 home, a 20% down payment comes to approximately $85,900, leaving you with a loan amount of $343,600. At today's rate of 6.47%, your estimated monthly principal and interest payment would be approximately $2,165.

Compare that to last week's rate of 6.52%, which would have resulted in a monthly payment of around $2,176. That's an $11-per-month difference — modest on its surface, but it adds up to $132 per year and over $3,900 across a 30-year loan term.

The more striking comparison comes when you stack today's rate against what buyers faced in June 2025, when the average 30-year rate was 6.81%. At that rate, the same $343,600 loan would have required a monthly payment of approximately $2,242. Today's buyers are saving $77 every month compared to buyers from a year ago — that's $924 annually and more than $27,700 over the life of the loan. Over time, those savings are anything but trivial.

Monthly Payment With a 3.5% Down Payment (FHA Loan)

Not everyone can swing a 20% down payment, and that's perfectly normal. For buyers using an FHA loan — which allows down payments as low as 3.5% — the numbers look different, but the rate-related savings are still significant.

On a $429,500 home, a 3.5% down payment equals roughly $15,033, leaving a loan balance of approximately $414,467. At the current 6.47% rate, the estimated monthly principal and interest payment rises considerably compared to the 20%-down scenario, reflecting the larger loan balance. FHA loans also typically require mortgage insurance premiums (MIP), which are not included in these base calculations but will increase your total monthly obligation.

Even so, the year-over-year rate improvement from 6.81% to 6.47% still delivers meaningful monthly savings for FHA borrowers — making this a more favorable borrowing environment than what buyers encountered in mid-2025.

Why Even Small Rate Drops Matter

One thing that often surprises first-time buyers is how much a fraction of a percentage point can affect long-term costs. A 0.34% reduction — the difference between this year's 6.47% and last year's 6.81% — doesn't sound like much. But on a $343,600 loan stretched over 30 years, it compounds into tens of thousands of dollars in total interest paid.

This is why timing matters, and why mortgage rate news is worth paying attention to even if you're not actively purchasing right now. Rate fluctuations affect not just your monthly payment but your overall purchasing power — and in a competitive summer housing market, that purchasing power can determine whether a particular home is within reach.

Key Factors That Affect Your Actual Rate

It's important to understand that the 6.47% rate cited by Freddie Mac is an average. The rate you're offered by a lender will depend on a variety of personal financial factors, including:

- Credit score: Borrowers with higher credit scores typically qualify for lower interest rates. A score above 740 usually unlocks the most competitive offers.

- Loan-to-value ratio (LTV): The more equity or down payment you bring, the less risk the lender takes on — which often translates to a better rate.

- Debt-to-income ratio (DTI): Lenders assess how much of your gross monthly income is committed to existing debts. A lower DTI signals stronger repayment capacity.

- Loan type and term: Conventional, FHA, VA, and USDA loans all carry different rate structures. A 15-year fixed loan will generally carry a lower rate than a 30-year fixed loan.

- Lender competition: Shopping around and comparing offers from multiple lenders — including banks, credit unions, and online lenders — can help you land a rate below the national average.

Should You Buy Now or Wait for Lower Rates?

This is the question on the minds of countless prospective buyers right now. The honest answer is that nobody can predict with certainty where rates will go next. What we do know is that today's rates are trending lower than they were a year ago, and that the housing market remains competitive with limited inventory in many areas.

Waiting for rates to fall further is a reasonable strategy for some, but it comes with trade-offs. Home prices could continue rising in the interim, and you may face more competition as more buyers re-enter the market if rates drop sharply. Many financial advisors suggest that if you find a home you love and can comfortably afford the monthly payment at today's rates, waiting may cost you more than you'd save.

A popular phrase in real estate circles is "marry the home, date the rate" — meaning you can always refinance later if rates improve, but you can't easily swap out the property itself.

Use a Mortgage Calculator to Run Your Own Numbers

Every buyer's financial situation is unique. The best way to understand what today's rates mean for you specifically is to use a mortgage calculator with your actual purchase price, down payment amount, and estimated loan term. Tools like the one available at Realtor.com allow you to plug in different scenarios and see exactly how your monthly payment shifts based on rate changes, down payment size, and loan amount.

Running these numbers before you start seriously shopping gives you a realistic sense of your budget — and puts you in a much stronger position when it's time to make an offer.

Bottom Line

Mortgage rates falling to 6.47% for the week of June 18, 2026 is a positive signal for the summer homebuying season. For a median-priced home at $429,500, a 20% down payment results in a monthly principal and interest payment of approximately $2,165 — $77 less per month than buyers were paying at this time last year. Whether you're putting down 3.5% through an FHA loan or bringing a full 20% to the table, today's rate environment is more favorable than it was in 2025. Use a mortgage calculator, get pre-approved, and talk to a lender to find out exactly where you stand.