Lower Asking Prices Are the Silver Lining for Buyers in an Otherwise Cloudy Housing Market

The 2026 housing market has been a challenging environment for most prospective homebuyers. Mortgage rates remain stubbornly elevated, economic uncertainty continues to weigh on consumer confidence, and inventory — while improving — has yet to reach levels that give buyers true negotiating power. Yet amid all of this, one consistent bright spot has emerged: asking prices are falling, and they have been falling for nearly five months straight.

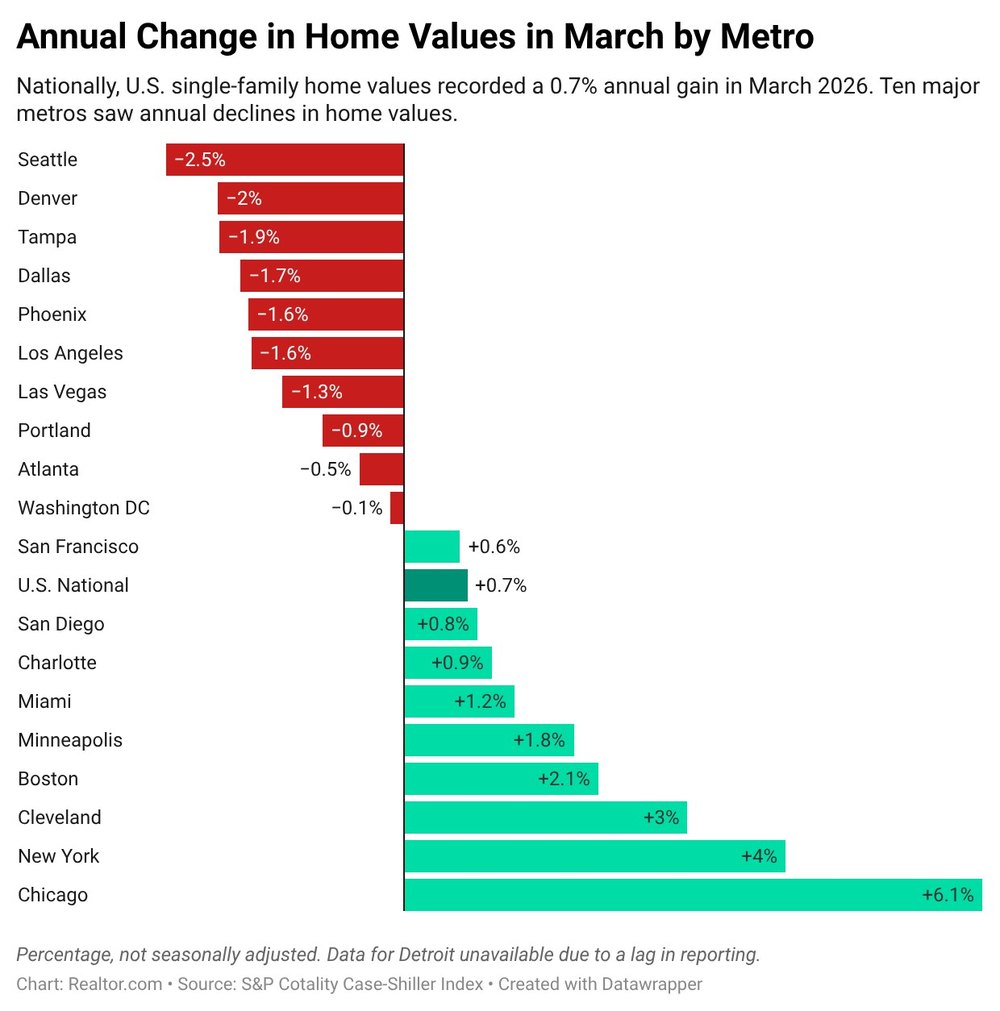

According to the latest weekly market update from Realtor.com's economic research team, the national median asking price for active listings was down 2.4% for the week ending May 23, 2026, compared to the same period one year earlier. More strikingly, this marks the 19th consecutive week of year-over-year asking price declines — the longest such streak recorded in at least a decade. For buyers who have been waiting on the sidelines, this trend may finally signal that the moment to act is approaching.

What's Driving the Decline in Asking Prices?

The drop in asking prices is not simply the result of a weakening economy or a sudden glut of distressed properties hitting the market. Instead, real estate economists point to a meaningful behavioral shift among sellers as the primary driver.

"More homes may be coming to market at realistic prices," says Hannah Jones, senior economist at Realtor.com. "Sellers appear to be listing at more modest prices from the start, rather than listing high and cutting later."

This shift is significant. In previous years, a common seller strategy was to list aggressively high, hoping to capture peak demand, and then gradually reduce the price over weeks or months if the home failed to sell. That approach burned time, frustrated buyers, and distorted market data. Today, more sellers appear to understand the current landscape and are pricing accordingly from day one — a development that creates a cleaner, more transparent market for everyone involved.

Several factors are encouraging this behavior change. Rising inventory means buyers have more alternatives, reducing the pressure to overpay on any single property. Additionally, homes that are overpriced are sitting on the market longer, which is a visible signal to other sellers that unrealistic pricing strategies are not working.

Are Lower Asking Prices Translating Into Lower Closing Prices?

One of the most important questions for buyers is whether these lower asking prices are actually translating into better final deals. The answer, increasingly, is yes — though not uniformly across all markets.

While final sales prices remain up slightly on a national basis compared to a year ago, Case-Shiller data released this week showed that more local markets are beginning to see downward pressure on closing prices as well. This lag makes sense: asking prices typically lead closing prices by several weeks or even months, since homes that are listed today will close weeks from now. If asking prices have been declining for 19 weeks, it is reasonable to expect that closing prices in many markets will begin to reflect this trend more fully in the months ahead.

For buyers, this means that the negotiating environment is improving. Sellers who have already priced realistically are more likely to accept reasonable offers without lengthy back-and-forth, reducing the time and emotional energy required to close a deal.

The Challenge That Remains: Mortgage Rates

Lower asking prices are genuinely good news, but they do not eliminate the affordability challenge that has defined this housing cycle. Mortgage rates remain elevated by historical standards, and the monthly payment on even a moderately priced home can stretch household budgets significantly.

To put this in concrete terms, consider a home listed at the national median price. Even a 2.4% reduction in asking price saves a buyer a meaningful sum on paper, but if the mortgage rate on a 30-year fixed loan is still hovering above 7%, the monthly carrying cost of that home remains high. Affordability, in other words, is a function of both price and financing costs — and the improvement on the price side has not yet been large enough to fully offset the burden of higher rates.

That said, buyers should not discount the value of lower asking prices entirely. Every percentage point of price reduction compounds over the life of a loan. A 2.4% price reduction on a $400,000 home represents roughly $9,600 off the purchase price, which translates into lower principal, lower monthly payments, and less interest paid over time.

What Should Buyers Do Right Now?

Given the current dynamics, buyers who are financially prepared should take the following considerations seriously as they evaluate their next move.

- Get pre-approved now: Knowing exactly what you can afford — and having documentation to prove it — puts you in a stronger position when you make an offer on a realistically priced home. Sellers who have already adjusted their expectations respond well to buyers who are clearly ready to close.

- Monitor price history carefully: With sellers increasingly pricing at market from day one, homes that still appear overpriced relative to comparables are worth watching. If they don't sell quickly, a price reduction — or a lowball offer — may be in order.

- Think long-term: Trying to perfectly time the housing market is nearly impossible. If you find a home that meets your needs at a price you can afford, the 19-week trend in your favor is an encouraging backdrop — not a reason to wait indefinitely for further declines.

- Explore rate buydowns: Some sellers in today's market are willing to offer concessions, including contributions toward mortgage rate buydowns, to attract qualified buyers. This is worth negotiating, as even a modest rate reduction can meaningfully lower your monthly payment.

- Work with a local expert: National data tells one story, but real estate is deeply local. A knowledgeable agent in your target market can tell you whether the national trend applies to the specific neighborhoods and price points you are considering.

The Broader Picture: A Market in Transition

The 19-week streak of declining asking prices is more than a statistical footnote. It represents a genuine recalibration of seller expectations after years of a market that heavily favored those listing homes. Sellers are no longer in a position to dictate terms, and buyers who have been patiently waiting are beginning to see the fruits of that patience.

At the same time, this is not a buyer's market in the classic sense. Inventory, while growing, remains below pre-pandemic norms in many areas. Competition for well-priced, move-in-ready homes can still be intense. And as long as mortgage rates remain elevated, the pool of buyers who can actually afford to purchase a home at current prices is constrained.

The most accurate description of today's housing market is one in transition — away from the extreme seller-dominance of 2021 and 2022, but not yet at the point where buyers hold all the cards. For buyers who are prepared, focused, and realistic about what they can afford, the current environment offers more opportunity than it has in several years. Lower asking prices are not a revolution, but they are a meaningful and welcome evolution in a market that has tested buyer patience for far too long.