Government Regulations Are Adding Over $131,000 to the Price of a New Home

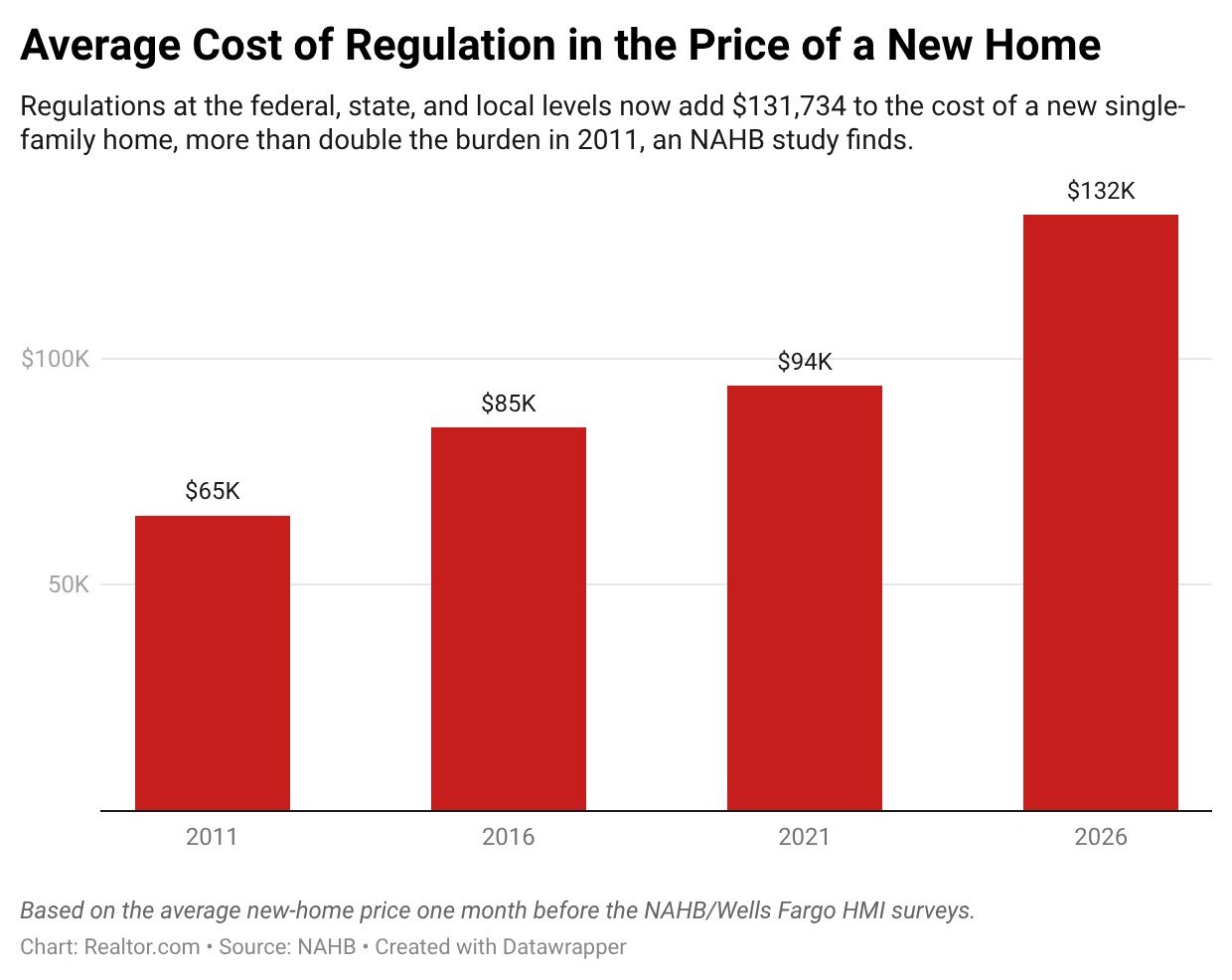

If you've been wondering why new homes feel increasingly out of reach, a major part of the answer may surprise you: it's not just land prices, labor shortages, or the cost of lumber. According to a new study from the National Association of Home Builders (NAHB), government regulations alone now account for more than $131,000 of the average new home's price tag — and that number has surged nearly 40% in just five years.

For millions of Americans already struggling to break into the housing market, this is a sobering reality. Regulatory costs now represent 26.4% of the average sales price of a new single-family home, which averaged $499,500 in January 2026. That means roughly one in every four dollars spent on a new home isn't going toward materials, craftsmanship, or land — it's going toward compliance with permits, building codes, inspections, and layers of government-mandated processes.

What the NAHB Study Revealed

The NAHB's 2026 special study on government regulation in the price of a home delivers a striking finding: regulatory costs have become one of the single largest drivers of new home prices in the United States. The study breaks down how these expenses accumulate throughout the homebuilding process, affecting everything from the lot development stage to the final certificate of occupancy.

According to the research, regulatory burdens fall into two broad categories:

- Regulations during development: These include costs associated with land use restrictions, zoning requirements, environmental impact studies, infrastructure mandates, and impact fees. They are incurred before a single nail is driven.

- Regulations during construction: These encompass building codes, inspection fees, energy efficiency mandates, permitting delays, and compliance with evolving federal, state, and local rules that builders must navigate to legally complete a home.

Combined, these two categories result in an average regulatory cost of $131,734 per new home — a figure that builders ultimately have no choice but to pass along to buyers.

Why This Matters for Housing Affordability

The United States is already facing a well-documented housing shortage. Studies have shown the country is short by millions of housing units, with demand from Millennials and Gen Z households continuing to outpace supply. Against that backdrop, the rising cost of regulation is adding fuel to an already dangerous fire.

NAHB Chairman Bill Owens put it bluntly: "This study illustrates how excessive regulation is deepening the nation's housing affordability crisis and making it harder for builders to deliver the affordable, attainable housing that our nation sorely needs."

The math is painful for prospective buyers. A household hoping to afford a median-priced new home at $499,500 — assuming a standard 20% down payment and a prevailing mortgage rate — would need a substantial income just to qualify. Strip away the $131,734 in regulatory costs, and that same home could theoretically be priced closer to $368,000, dramatically expanding the pool of Americans who could afford homeownership.

Of course, eliminating all regulatory costs overnight is neither realistic nor desirable — some regulations exist to protect public safety, environmental quality, and neighborhood integrity. But the sheer scale and pace of growth in these costs raises legitimate questions about whether the regulatory environment has become bloated beyond what public benefit justifies.

The 40% Surge: A Five-Year Look

Perhaps the most alarming detail in the NAHB study is not the absolute dollar figure, but the rate of growth. Regulatory costs have jumped nearly 40% over just five years. That pace far outstrips general inflation and wage growth, meaning the regulatory burden is consuming an ever-larger share of household income relative to what buyers can actually afford.

This trajectory, if unchecked, threatens to make new home construction increasingly unviable at price points accessible to working- and middle-class Americans. Builders operating in tight markets are already walking away from entry-level projects because the cost structure simply doesn't pencil out. The result is a market that continues to skew toward higher-end construction, leaving first-time buyers further behind.

What Needs to Change: The Case for Regulatory Reform

Owens and the NAHB are calling on policymakers at all levels of government to take action. "Policymakers should remove unnecessary and costly regulations that are pricing buyers out of the market and slowing construction of new homes and apartments," Owens urged.

Specific reforms that housing advocates and industry groups have long championed include:

- Streamlining the permitting process: Lengthy permitting timelines don't just cost money in fees — they tie up capital, delay projects, and increase carrying costs for builders, all of which inflate final prices.

- Reforming zoning laws: Restrictive single-family zoning in high-demand areas limits housing density and drives up land costs. Allowing more mixed-use and multifamily development can meaningfully increase supply.

- Reviewing impact fees: While impact fees fund important infrastructure, some jurisdictions have imposed fees that are disproportionate to actual infrastructure needs, effectively acting as a tax on new housing.

- Reducing duplicative inspections and code requirements: In many markets, builders must navigate overlapping local, state, and federal requirements that serve similar purposes but require separate compliance costs.

The Bottom Line for Homebuyers and the Market

For anyone currently trying to buy a home — or planning to in the coming years — the NAHB study is an important reminder that the housing affordability crisis is not solely the product of market forces. Policy choices have real consequences, and the regulatory environment surrounding new home construction has quietly become one of the most significant barriers between Americans and homeownership.

Until meaningful reform takes hold, builders will continue passing these costs downstream to buyers. And as long as regulatory burdens keep climbing at their current pace, the dream of affordable new housing will remain frustratingly out of reach for a growing share of the population. The conversation about housing costs must include a serious, sustained focus on red tape — because right now, that red tape is costing the average buyer over $131,000 before they even turn a key in the door.