The First of the Month Just Got a Digital Makeover

For millions of renters, the first of the month has long meant the same thing: dig out the checkbook, scribble a payment for a painfully large sum, and hand it off to a landlord. It's a ritual as old as modern renting itself. But for the first time in history, that routine now belongs to the minority. In 2025, online rent payments officially surpassed offline payments, marking a turning point in how Americans meet one of their most fundamental financial obligations.

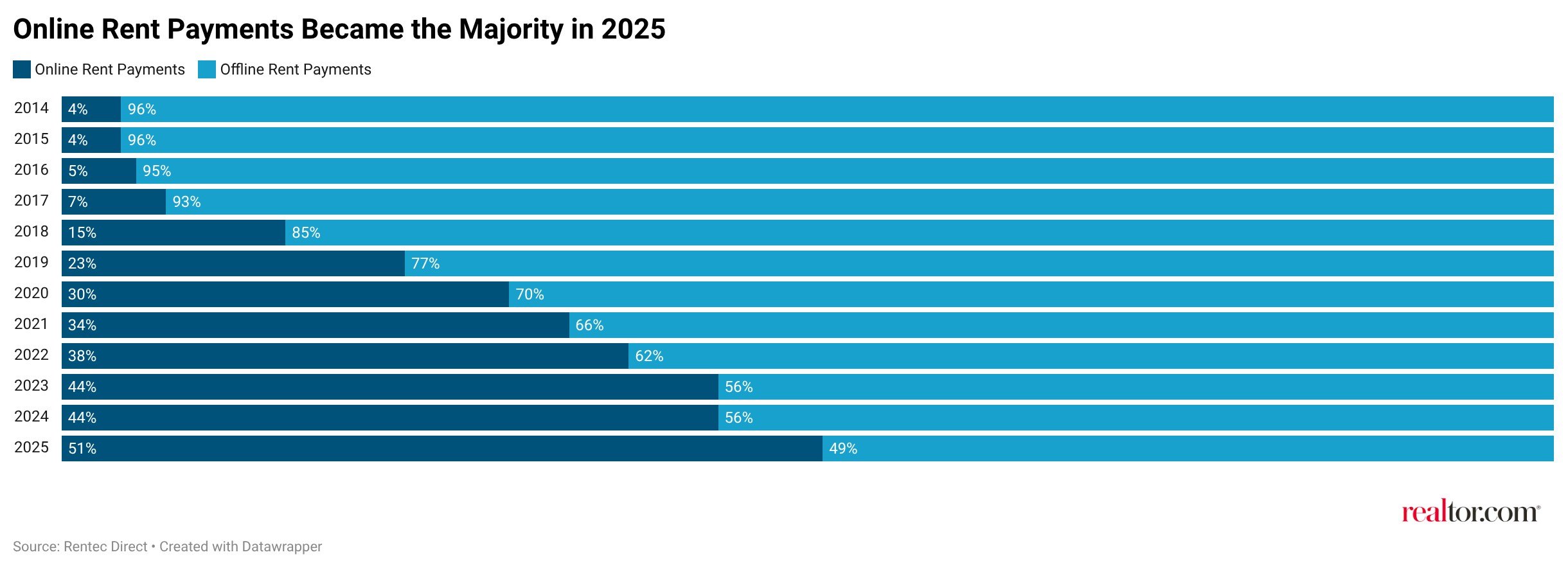

According to a landmark report from Rentec Direct, a property management software company, just 49% of renters still pay rent by check or cash. The remaining 51% now pay online — a seismic shift from just a decade ago, when digital rent payments accounted for a mere 4% of transactions. The study analyzed ten years of rental data drawn from 1.2 million renters and more than $21 billion in payments, making it one of the most comprehensive looks at rent payment behavior ever conducted.

Why Rent Took So Long to Go Digital

The slow migration of rent payments to the internet might seem surprising in an era when you can tap your phone to buy coffee, split a restaurant bill instantly, or pay a utility bill in seconds. By 2015, roughly 10% of all consumer transactions were already taking place online or remotely, according to the Federal Reserve's Diary of Consumer Payment Choice. Yet at that same point in time, only about 4% of rent payments were being made digitally.

Several factors explain this lag. Rent is not a typical consumer transaction. It involves large sums of money, legal agreements, and a long-term relationship between two parties — often individuals rather than corporations. Many small and independent landlords were slow to adopt property management technology, either due to cost concerns, a preference for paper trails, or simple unfamiliarity with digital tools.

Trust also played a significant role. Tenants handing over a month's rent online had to be confident in the security of the platform and the reliability of the transaction record. Unlike buying a book on Amazon or streaming a movie, there is no easy "undo" button when a rent payment goes wrong. The stakes are higher, and both parties tend to approach the process with corresponding caution.

Additionally, the rental market has historically skewed toward lower-income households, a demographic that has faced disproportionate barriers to digital financial services, including limited access to bank accounts and broadband internet. These structural gaps slowed the adoption of online rent payment among a meaningful portion of the renter population.

What Changed to Accelerate the Digital Shift

The COVID-19 pandemic served as a powerful accelerant for digital adoption across virtually every sector of the economy, and rent was no exception. When in-person contact became dangerous or impossible, both landlords and tenants were pushed to find contactless alternatives. Online rent payment platforms — many of which had existed for years without widespread uptake — suddenly became essential infrastructure.

At the same time, the broader expansion of smartphones and affordable internet access brought more households into the digital economy. Payment apps became easier to use, more secure, and more widely trusted. Property management software companies invested heavily in user-friendly interfaces that made online rent payment accessible even to less tech-savvy users.

For landlords managing multiple units, the business case for digital payments became increasingly hard to ignore. Automated payment tracking, instant confirmation, and reduced administrative overhead made online systems not just convenient but genuinely superior to paper-based methods. The efficiency gains alone were enough to motivate widespread landlord adoption, which in turn nudged tenants toward digital options.

What the Shift Means for Renters

The move to online rent payments carries real, tangible consequences for tenants. On the positive side, digital payments offer convenience, speed, and a clear electronic record of every transaction. Renters no longer need to schedule their lives around office hours or worry about a check getting lost in the mail. Automatic payments can eliminate the risk of late fees caused by simple forgetfulness.

However, the digital shift is not without its complications. Some online platforms charge processing fees that effectively increase the monthly cost of rent. ACH bank transfers are often free or low-cost, but credit card payments can carry fees of 2% to 3% — a meaningful amount on a payment of $1,500 or more. Renters who rely on credit card payments to manage cash flow may find themselves absorbing those costs quietly, month after month.

There are also concerns about data privacy and the growing volume of financial information flowing through third-party platforms. When rent payments move through software intermediaries, those companies collect detailed data about payment behavior — data that could, in theory, be shared, sold, or used in ways renters may not fully anticipate or understand.

What the Shift Means for Landlords

For property owners, the digitization of rent collection is largely a positive development, but it comes with its own set of adjustments. Landlords who have long relied on checks and cash may need to invest in new systems, learn new software, and update their lease agreements to reflect digital payment expectations. Smaller landlords, in particular, may find the transition more demanding than their larger, institutional counterparts.

On the upside, digital payment records simplify bookkeeping, streamline tax preparation, and reduce the friction associated with late payment follow-ups. Automated reminders and payment portals shift some of the responsibility for on-time payment to renters themselves, potentially reducing landlord stress and improving cash flow predictability.

The Holdouts and the Road Ahead

With 49% of renters still paying by check or cash, it would be premature to declare the rent check dead just yet. That figure represents tens of millions of households across the country, and their reasons for sticking with traditional payment methods are varied and often deeply rooted in circumstance rather than preference.

Some renters remain unbanked or underbanked, lacking the accounts required to participate in most digital payment systems. Others live in rental arrangements — particularly informal ones — where paper payment remains the norm by mutual agreement. And some simply value the tangible, irreversible nature of a physical check in a way that digital alternatives have not yet replicated.

What is clear is that the direction of travel is firmly toward digital. The 47-percentage-point surge in online rent payments over the past decade — from 4% in 2014 to 51% in 2025 — represents one of the most rapid behavioral shifts in American financial life. As technology continues to improve and access barriers continue to fall, the share of renters still reaching for a checkbook on the first of the month will almost certainly keep shrinking. The rent check isn't dead yet, but its days are numbered.