Mortgage Rates Drop to 6.48%: What It Means for Today's Homebuyers

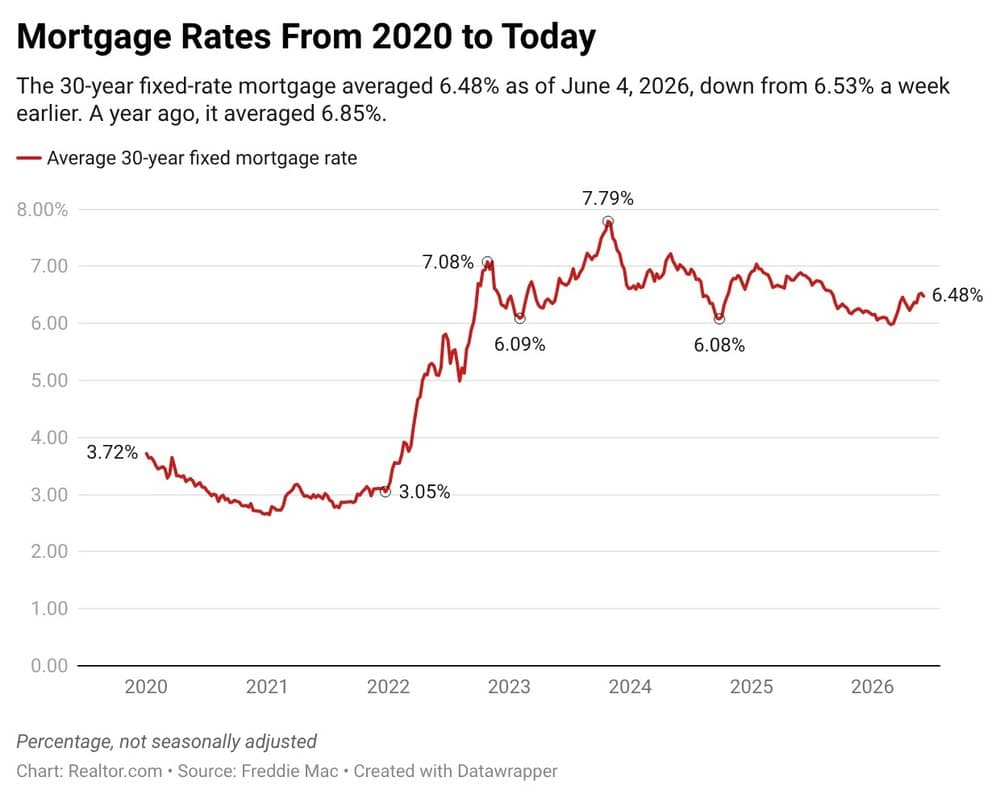

After weeks of elevated borrowing costs, mortgage rates finally showed signs of relief in early June 2026. According to Freddie Mac, the average rate on a 30-year fixed home loan fell to 6.48% for the week ending June 4, 2026 — a five-basis-point decrease from 6.53% the prior week. The retreat was largely driven by easing global energy prices following an uneasy ceasefire between the U.S. and Iran, which cooled pressure on bond markets and, in turn, on borrowing costs.

For context, this same time last year — June 2025 — rates averaged 6.85%. That difference may not sound dramatic, but as we'll show below, even a fraction of a percentage point can translate into meaningful savings over the life of a 30-year loan. If you've been sitting on the sidelines waiting for rates to dip, now is a good moment to run the numbers.

Using a standard mortgage calculator, we've broken down exactly what it costs to buy a home at the current national median price of $415,000 under today's rate environment. All examples assume a 30-year fixed mortgage and include principal and interest only. Property taxes, homeowners insurance, and private mortgage insurance (PMI) are not included in these figures.

Monthly Payment With a 20% Down Payment

A 20% down payment on a $415,000 home means putting $83,000 down upfront, leaving a loan balance of $332,000. At today's rate of 6.48%, your estimated monthly principal and interest payment comes to approximately $2,094.

Compare that to last week's payment of $2,105 — you're already saving $11 per month. But the bigger story is the year-over-year comparison. At June 2025's average rate of 6.85%, the same loan would have cost $2,175 per month. That's a savings of $81 every month, or roughly $972 per year. Over a full 30-year loan term, that difference compounds to nearly $29,160 in total interest savings.

For buyers who have the financial flexibility to put 20% down, this rate environment offers a genuine window of opportunity — especially compared to the elevated costs that defined much of 2025.

Monthly Payment With a 3.5% Down Payment (FHA Loan)

Not every buyer can afford a 20% down payment, and that's completely normal. FHA loans allow qualified buyers to put as little as 3.5% down, making homeownership more accessible for first-time buyers and those still building their savings.

On a $415,000 home, a 3.5% down payment equals $14,525 — significantly more achievable for many households. That leaves a loan amount of $400,475. At the current 6.48% rate, the estimated monthly principal and interest payment on this loan is approximately $2,519.

It's worth noting that FHA loans typically require mortgage insurance premiums (MIP), which will add to your total monthly cost. Buyers should factor this in when budgeting, as MIP can add anywhere from $100 to $200 or more to the monthly payment depending on the loan amount and term.

Still, for buyers who qualify, putting only 3.5% down can make the difference between renting and owning — especially in a market where home values continue to hold steady.

Monthly Payment With a 10% Down Payment

A 10% down payment is a popular middle ground for buyers who want to reduce their loan balance without depleting their savings entirely. On a $415,000 home, that's $41,500 down, resulting in a loan of $373,500.

At 6.48%, the estimated monthly payment on this loan is approximately $2,352 in principal and interest. Buyers at this level may still be subject to PMI until they reach 20% equity in the home, which is an important cost to factor into your overall budget.

How Geopolitics Are Shaping Mortgage Rates Right Now

The recent dip in mortgage rates wasn't driven by Federal Reserve policy — it was the bond market reacting to geopolitical developments. The U.S.-Iran ceasefire eased concerns about a sustained spike in global oil prices, which had been putting upward pressure on inflation expectations and, by extension, on the 10-year Treasury yield that mortgage rates closely track.

This is a reminder of just how interconnected global events and everyday financial decisions have become. A ceasefire thousands of miles away can shave dollars off your monthly mortgage payment. Of course, this also means rates can rise again quickly if tensions escalate or new economic data surprises the market.

Should You Buy Now or Wait for Rates to Fall Further?

This is the question on every prospective buyer's mind. The honest answer is: it depends on your individual circumstances. Here are a few key considerations to weigh:

- Rate uncertainty is real. Rates have been volatile in 2025 and 2026. There's no guarantee they'll fall further — they could just as easily rise back above 6.5% or higher if inflation rebounds or geopolitical tensions intensify.

- Home prices aren't waiting. The national median sits at $415,000 and inventory remains tight in many markets. If prices continue to rise, waiting for a slightly better rate could mean paying significantly more for the same home.

- You can refinance later. One common strategy is to buy now at the current rate and refinance if and when rates decline more substantially. This lets you lock in a home at today's prices while keeping the door open for lower payments in the future.

- Run your own numbers. Every buyer's financial situation is different. Use a mortgage calculator to model your specific down payment, loan amount, and rate scenario before making any decisions.

The Bottom Line

A 6.48% mortgage rate is not historically low, but it represents a meaningful improvement from where rates stood just a year ago. For a buyer purchasing a $415,000 home today with 20% down, the monthly payment of $2,094 is $81 less than it would have been in June 2025 — real money that adds up quickly over time.

Whether you're a first-time buyer exploring FHA options or a move-up buyer ready to put 20% down, understanding what today's rates actually mean for your wallet is the first step toward making a confident, informed decision. The market is never perfect, but the math is always worth knowing.